Help CleanTechnica’s work by a Substack subscription or on Stripe.

After the December end-of-incentive gross sales rush (NEVs are not exempt from buy tax this yr), and the next gross sales hunch, excessive gasoline costs and a by no means ending wave of latest fashions has allowed April to achieve file EV market share, with plugins surpassing the 60% barrier for the primary time!

However whereas up to now it was achieved due to file EV gross sales, this time, that is due to a big ICE (inside combustion engine) crash. The general market dropped 22% yr over yr (YoY), to round 1.4 million gross sales. ICE-powered fashions had been on the epicenter of this disruption, crashing 37% YoY, however plugin hybrids (PHEVs) had been additionally down 25% in April, and even extended-range electrical autos (EREVs) dropped, albeit a extra reasonable 11% YoY.

The one factor that grew in April? Pure electrics. Regardless of having fewer incentives, BEVs had been up 2% YoY, to 579,000 gross sales. So, this meant that BEVs scored a file 42% BEV share in China!

Including PHEVs (13% share) and EREVs (6%) to the tally meant that in April a file 61% of all vehicles offered in China had a plug!

This consequence pulled the 2026 share to 49% (in the identical interval final yr, it was at 48% share). BEVs on their very own had been additionally up, to 32% (30% BEV in Jan–April ’25). Anticipate to see plugins north of the 50% mark, and BEVs over 33%, on the finish of the primary half of the yr.

One other fascinating statistic is that the breakdown between pure electrics and plugin hybrids is shifting, to the revenue of BEVs. In the beginning of the yr, PHEVs had been benefiting from the incentive-derived BEV drop, however pure electrics are returning with a vengeance. April confirmed a 68% vs. 32% breakdown, to the advantage of BEVs, considerably above the 65%/35% common of 2026.

Having a fast take a look at Chinese language exports — even right here plugins are breaking new floor. EV share scored a file 53%, or 406,000 models, in April alone. And with Chinese language OEMs quick profitable share abroad, markets the place they’re current in giant volumes are additionally being shortly electrified….

All these disruptions are seen within the general rating. Within the first months of the yr, ICE fashions had been populating the highest positions, however April noticed them decreased to only one consultant, and it was solely in ninth (the small Geely Binyue).

Which additionally meant that there have been no representatives from overseas legacy OEMs among the many prime 10 fashions within the general market in China…. Yep, there is no such thing as a solution to conceal the massacre anymore.

Six years in the past, the Chinese language prime 10 was product of 6 overseas legacy OEM fashions (1 Nissan, 3 Volkswagens, 1 Toyota, and 1 Buick), subsequent to 4 fashions from native manufacturers (2 Geely, 1 Haval, and 1 Changan). Now the perfect promoting mannequin from a overseas legacy model is just … nineteenth general (VW Lavida).

And whereas overseas manufacturers nonetheless characterize a sizeable chunk of the disappearing ICE gross sales, trying simply at plugins, native manufacturers already characterize 80% of gross sales! If nothing is finished to revert this pattern, in 4 years, overseas manufacturers may personal simply 20% of the Chinese language automotive market!

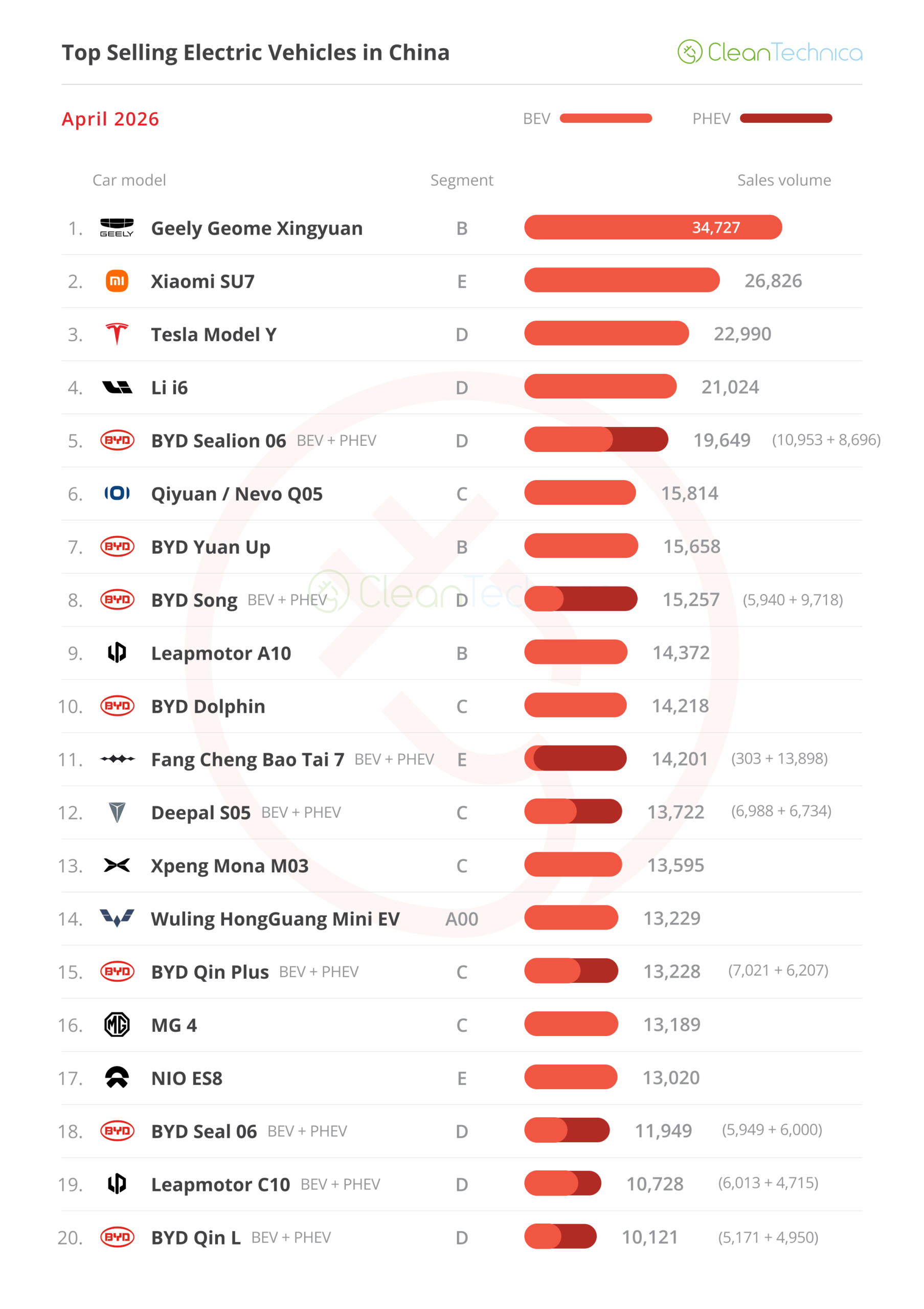

One other pattern is the BEV push being fairly seen within the prime 10. The highest 4 fashions are pure electrics, and seven out of the ten fashions on the desk are BEVs, with the remaining being one ICE mannequin and two combined fashions (BEV+PHEV).

With this in thoughts, it’s solely a query of time till we see a 100% plugin prime 10 (June?), with the following query now being: When will we see a totally BEV prime 10?

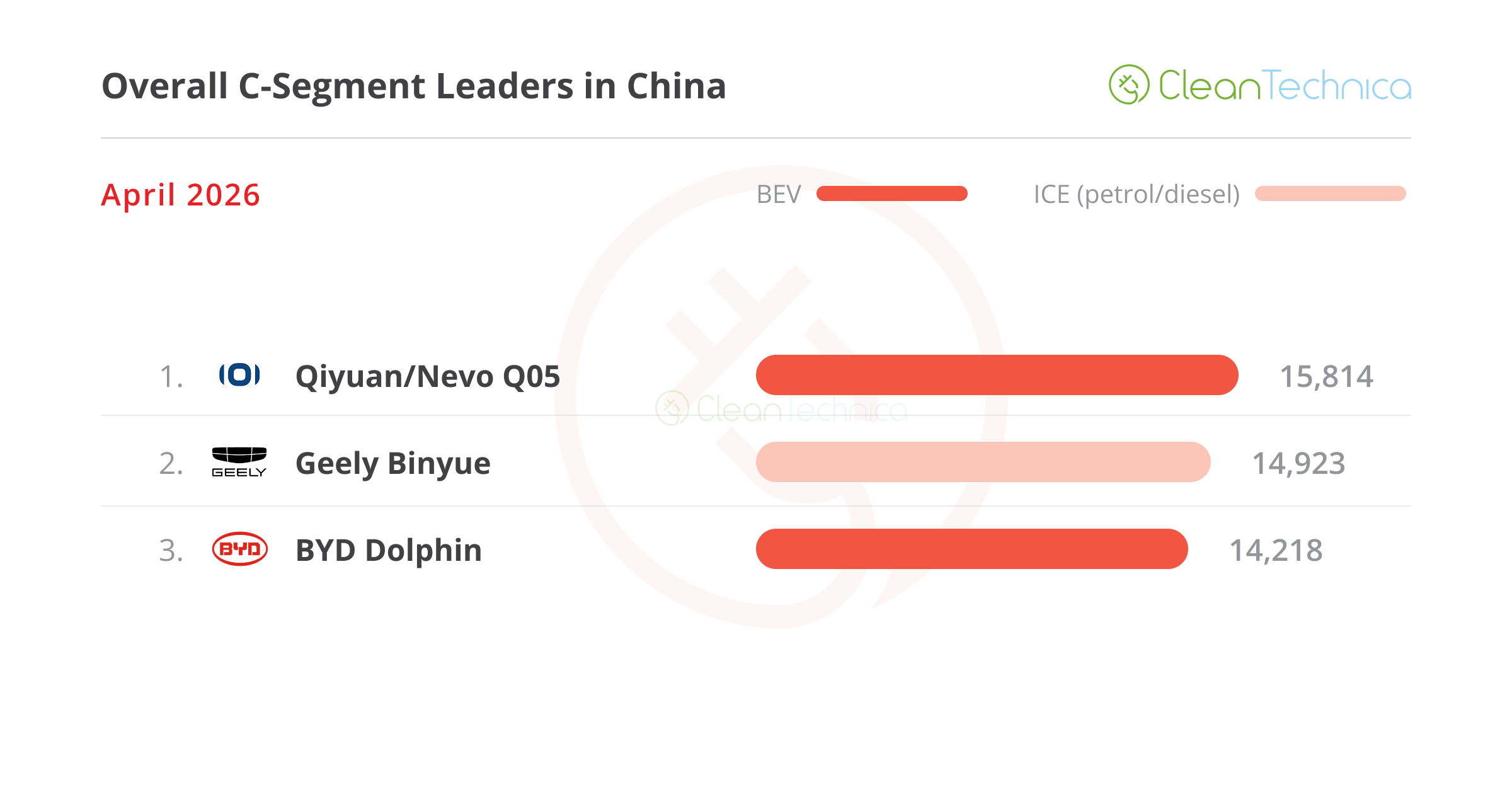

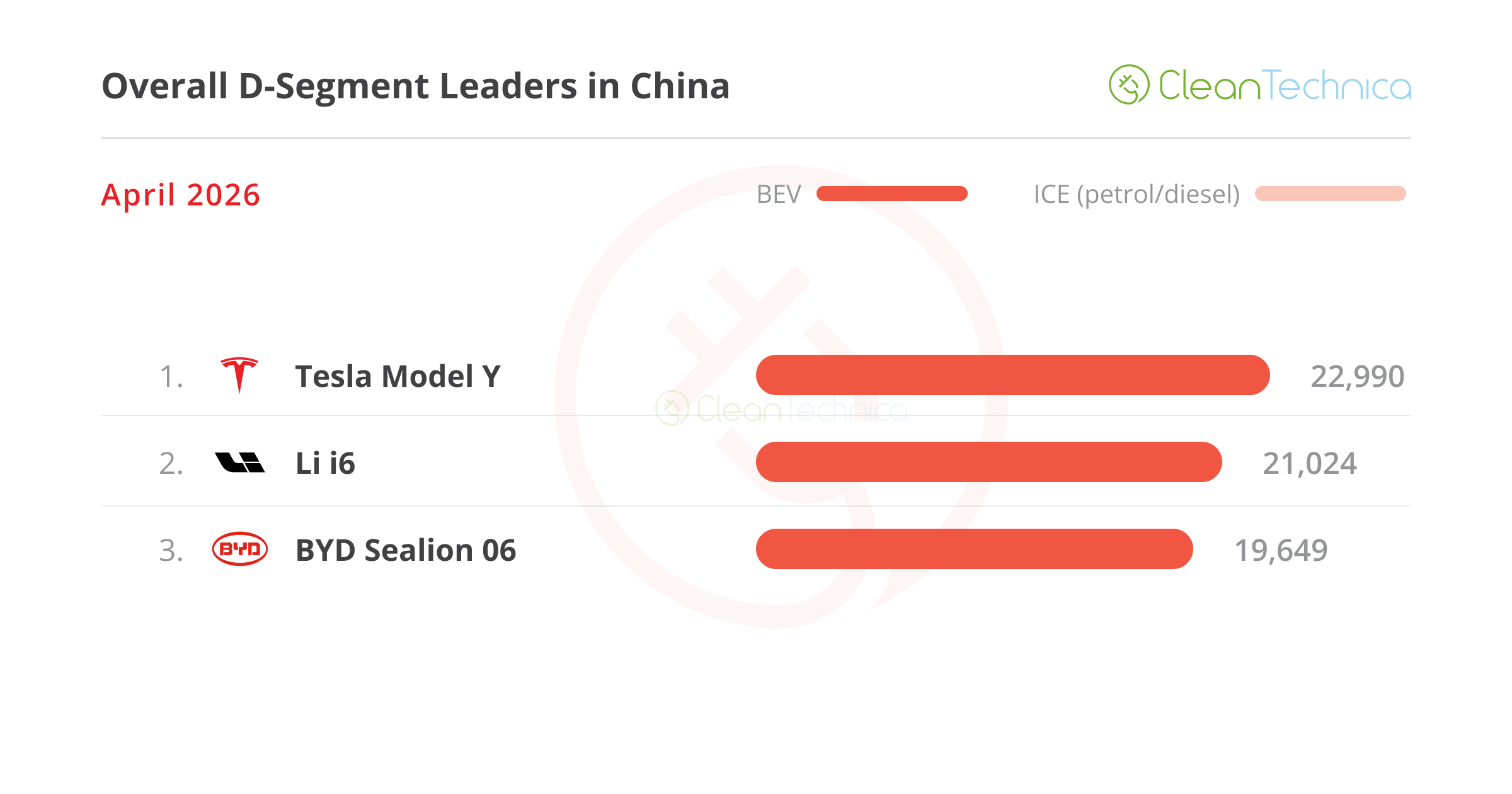

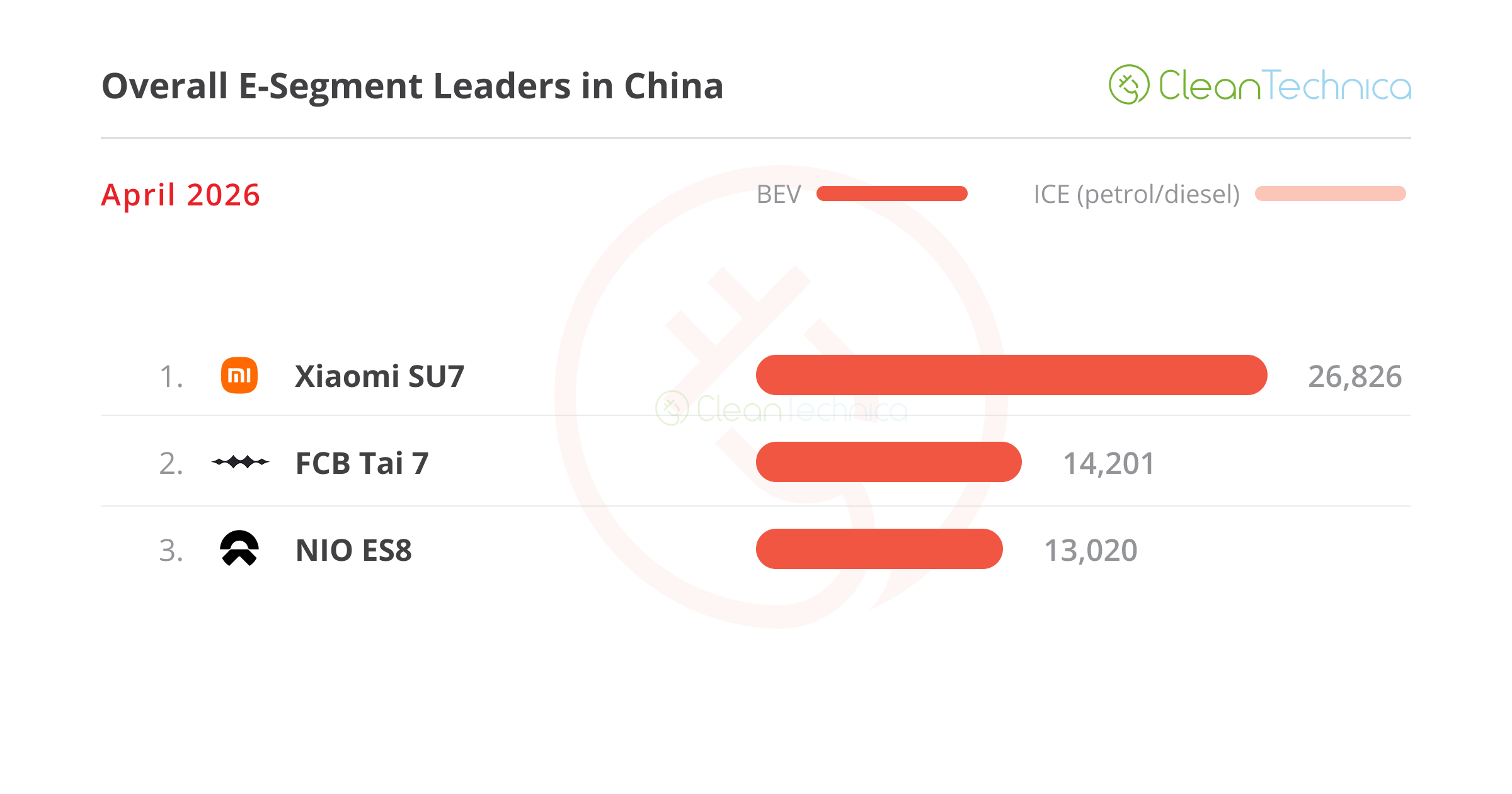

Taking a look at the perfect sellers in a number of dimension classes, the EV push can also be fairly seen, as even the C-segment (compact vehicles) has a BEV majority. Actually, there was just one ICE mannequin in all 5 classes (the Geely Binyue, within the C section). As such, it’s solely a query of time till ICE fashions are faraway from all of the podium positions, with the following goal now being eradicating combined powertrain (BEV+PHEV) fashions.

Additionally, a word for policymakers in China: the class most affected by the subsidy reduce was metropolis vehicles, with the class having dismal outcomes since then. Solely the Wuling Mini EV has offered in half-decent numbers. Simply to offer an thought of the gross sales drop, this month’s third positioned Changan Lumin scored fewer than 3,000 models, whereas in the identical month a yr in the past, it had 13,000 … and wasn’t even on the rostrum! Possibly it could be a good suggestion to create some form of Kei-car class to revive gross sales of metropolis vehicles?

Taking a look at particular person fashions, the most important shock was the Xiaomi SU7 profitable the complete dimension class. Due to a current refresh, Xiaomi’s sporty sedan left its rivals, together with its YU7 sibling, within the mud. Will this be a one-time factor, or is the SU7 again for good?

Right here’s extra information and commentary on April’s prime promoting electrical fashions:

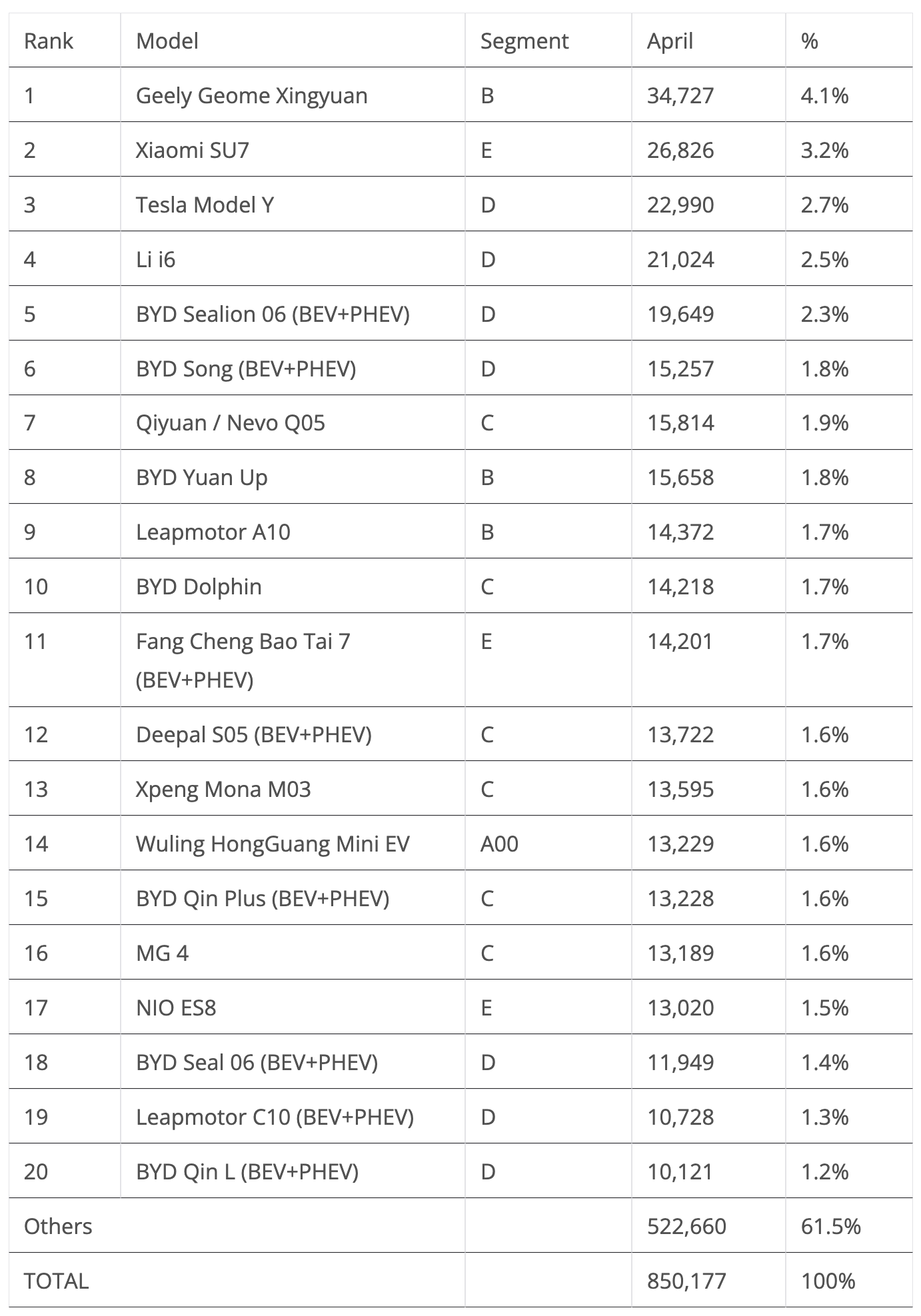

#1 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull cash ($10,000 USD). At the very least, that’s how Geely’s inside memo might need described the Geome Xingyuan when growing its newest hatchback. And it’s bought an fascinating identify, as Xingyuan interprets as “wishing upon a star.” Plainly Geely had its want granted. The small hatchback has lastly given the Hangzhou OEM the a lot coveted Greatest Vendor standing, not solely beating its BYD nemesis but additionally the remainder of the competitors. In April, the Geely mannequin was #1, with 34,727 registrations, which represented a slight 4% drop. With the main focus now being in export markets, the small hatchback is now at cruising velocity, in its residence market.

#2 — Xiaomi SU7

The poster youngster of the Chinese language EV market joined the highest 5 in April due to 26,826 registrations, a 6% drop in comparison with the identical month final yr. This was its finest lead to 11 months nonetheless, due to the current refresh. That implies that it was the perfect promoting sedan in China, simply behind the less expensive Geely Xinguyan. With a Porsche Taycan–like design, however for Tesla Mannequin 3 cash, the startup’s EV success is simple. Having mentioned that, it has loads of peaks and valleys, not not like a former US startup….

#3 — Tesla Mannequin Y

The prolonged wheelbase model, imaginatively referred to as “L,” helps the Mannequin Y’s fortunes in China. In April, deliveries had been up by 15% YoY, to 22,990 models. The lengthy wheelbase model is proving to be an actual lifeline for the US crossover, preserving the Mannequin Y’s gross sales afloat — particularly in comparison with its sibling Mannequin 3. With simply 3,000 deliveries final month, the Mannequin 3 has seen its gross sales drop to lower than half of what they had been in April 2025.

#4 — Li Auto i6

After a powerful begin to the yr, issues proceed to go effectively for the midsize mannequin, with the startup EV securing one other prime 5 presence due to 21,024 registrations. With a excessive quantity of area, consolation, and luxurious for simply $35,000 USD (for reference, the most affordable Tesla Mannequin Y in China begins at $36,000 USD), the i6 presents an intensive record of kit (air suspension, fridge, superior self-driving — together with Lidar). It additionally has a powerful concentrate on area (three-meter wheelbase) and luxury. It’s a mannequin that provides full dimension luxurious in a midsize-priced EV.

#5 — BYD Sealion 06 (BEV+PHEV)

BYD’s new midsize crossover scored 19,649 registrations, permitting it to win one other prime 5 standing. With the BYD Track in a transitional stage, as the brand new, flash-charging succesful, Extremely physique is ramping up, the Sealion 06 is BYD’s present breadwinner on this home market. It’s positioned at round 150,000 CNY (round $22,000) and has the usual BYD qualities of worth for cash, design, and connectivity. On the EV specs facet, the PHEV model has an above-average 27 kWh battery, and the BEV model’s prime battery has an unimpressive 79 kWh. Additionally, the 800V structure is a plus at this value level. Which means the Sealion 06 has sufficient worth for cash to have a superb profession, however it’s no star participant.

Taking a look at the remainder of the perfect vendor desk, let’s see what the highlights present.

A mannequin on the rise is the #7 Qinyuan/Nevo Q05, with Changan’s mainstream EV model benefiting from a brand new era of its compact crossover to attain a file 15,814 registrations, its second file lead to a row! Equally, its premium cousin, the Deepal S05, had one other desk presence, twelfth place, highlighting a optimistic month for the Chongqing OEM.

The opposite main spotlight is Leapmotor’s new child, the small A10 crossover, which surged to ninth in solely its second month available on the market. It scored 14,372 gross sales. Is that this the perfect vendor that the startup was ready for?

Exterior the highest 20, a Toyota mannequin deserves a point out. The BZ3X compact crossover scored 10,027 gross sales in April, its finest lead to 9 months. Is Toyota lastly waking up?

April introduced a variety of related landings, with the three most necessary ones being:

- A brand new Chery QQ3 EV. In contrast to its predecessor, which gained the Greatest Vendor title in China on two totally different events (2011 and 2013), the brand new QQ3 is not a tiny metropolis automotive remodeled into an affordable, however not cheerful, EV. The brand new one was created from scratch to run with the perfect of BYD (Seagull and Dolphin) and Geely (Xingyuan). With an fascinating design, a budget and cheerful Chery landed with related quantity (8,494 models), so a prime 20 place appears seemingly. Will it be capable of run with the perfect of Geely and BYD?

- Leapmotor has gotten Land Yacht Fever and launched the D19. Nearly 5.3 meters lengthy, which is Cadillac Escalade-like, the 80 kWh battery is the most important ever fitted into an EREV, which form of begs the query: Why would you need an ICE engine on prime of a 80 kWh battery? Anyhow, it has one, in addition to a 0–100 km/h time of three seconds (once more — why?…). All of this extra comes for the value of simply US$33,000…. (With examples like this, no surprise US makers wish to preserve Chinese language OEMs out of their home market.) It landed with 4,455 gross sales.

- Nonetheless in Land-yacht-stan, we have now the VW ID.ERA 9X. Volkswagen’s tackle the XXXL EV SUV, the 9X is simply a few centimeters smaller than the aforementioned Leapmotor D19, so nonetheless Cadillac Escalade-like. And it’s primarily based on a SAIC platform (IM Motors, to be exact), therefore being the primary EREV mannequin for the model. With a alternative of 51 and 65 kWh batteries, it has the same old lengthy electrical vary + ICE vary, in addition to the obligatory luxuries of the class. Now the value — it begins at US$45,000. So, this or the longer vary, US$12,000 cheaper Leapmotor D19? Hmm … robust alternative, isn’t it? No surprise the massive Volkswagen has landed with nearly half of the registrations (2,326) that the Leapmotor had….

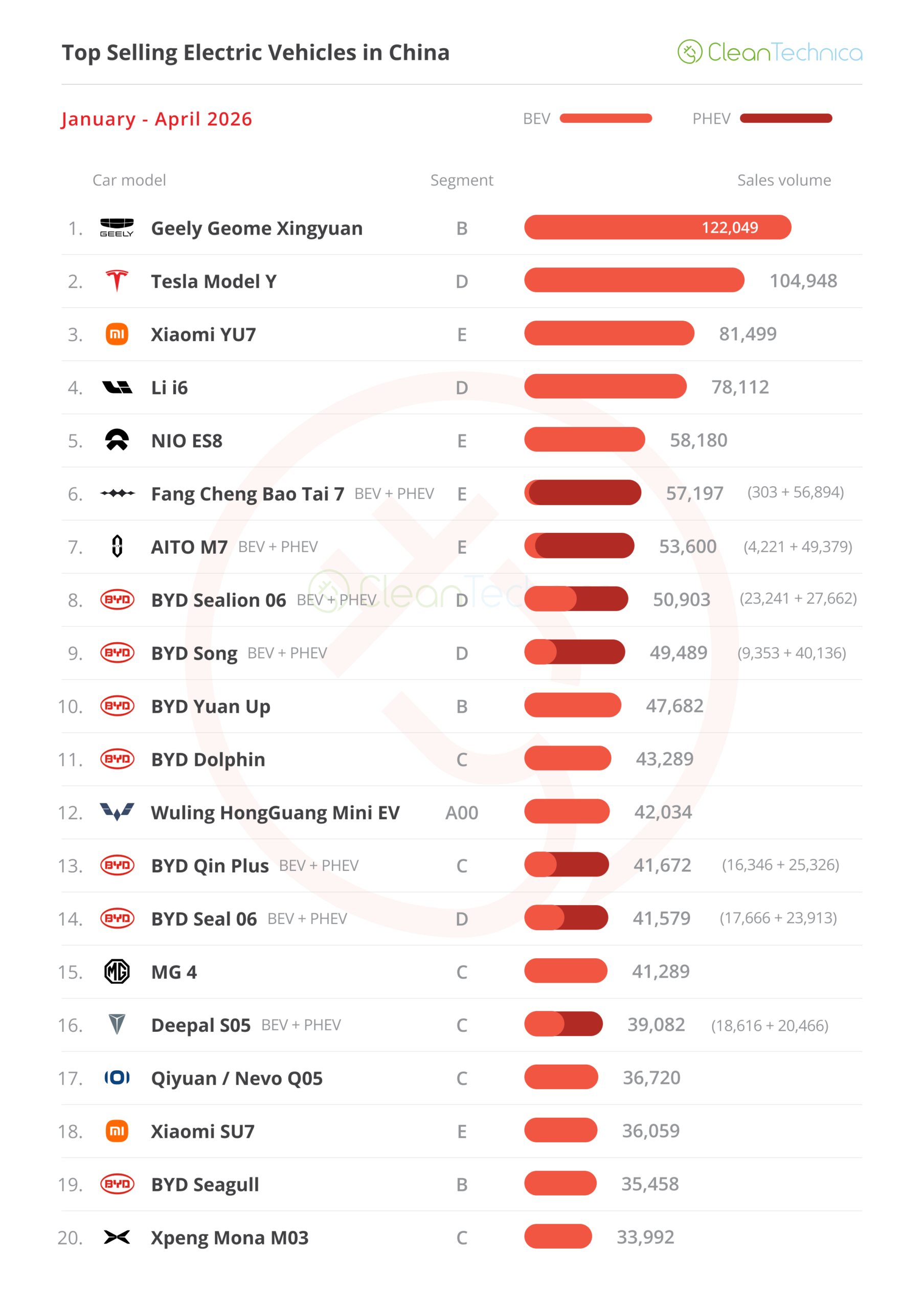

Wanting on the 2026 rating, there have been no main modifications on prime. Though, the Xiaomi YU7 had a sluggish month, which implies that the sporty crossover is now being intently adopted by the #4 Li i6.

Under the rostrum positions, benefiting from one other sluggish month from the AITO M7, the Fang Cheng Bao Tai 7 surpassed it and is now sixth, fewer than 1,000 models behind the fifth positioned NIO ES8.

Nonetheless within the BYD steady, the Sealion 06 climbed one other place, into eighth, whereas the BYD Dolphin was as much as eleventh and the outdated canine BYD Qin Plus jumped two spots to #13.

But it surely wasn’t solely BYDs that had been on the rise. One must also spotlight the MG 4 climbing to #15, and the Deepal S05 going up two positions to #16.

And the final positions noticed three new entries. On prime of the Deepal S05, Changan now additionally has the Qiyuan/Nevo Q05 on the desk, becoming a member of it at #17. In the meantime, the Xiaomi SU7 returned to the highest 20, at #18, permitting Xiaomi to have each of its fashions on the desk.

Lastly, XPENG positioned its Mona M03 finest vendor again on the desk, in twentieth.

For these new fashions to hitch, others needed to go away the desk, with one in all them being … the Tesla Mannequin 3. Yep, now the Tesla Mannequin Y is the one overseas mannequin on the desk. Positive, the Mannequin 3 will return, most likely in June, however with gross sales down 46% YoY, the destiny of the Tesla sedan into oblivion appears sure. And to suppose {that a} yr in the past, the Texan was ninth in China…. Now, not even a prime 20 spot.

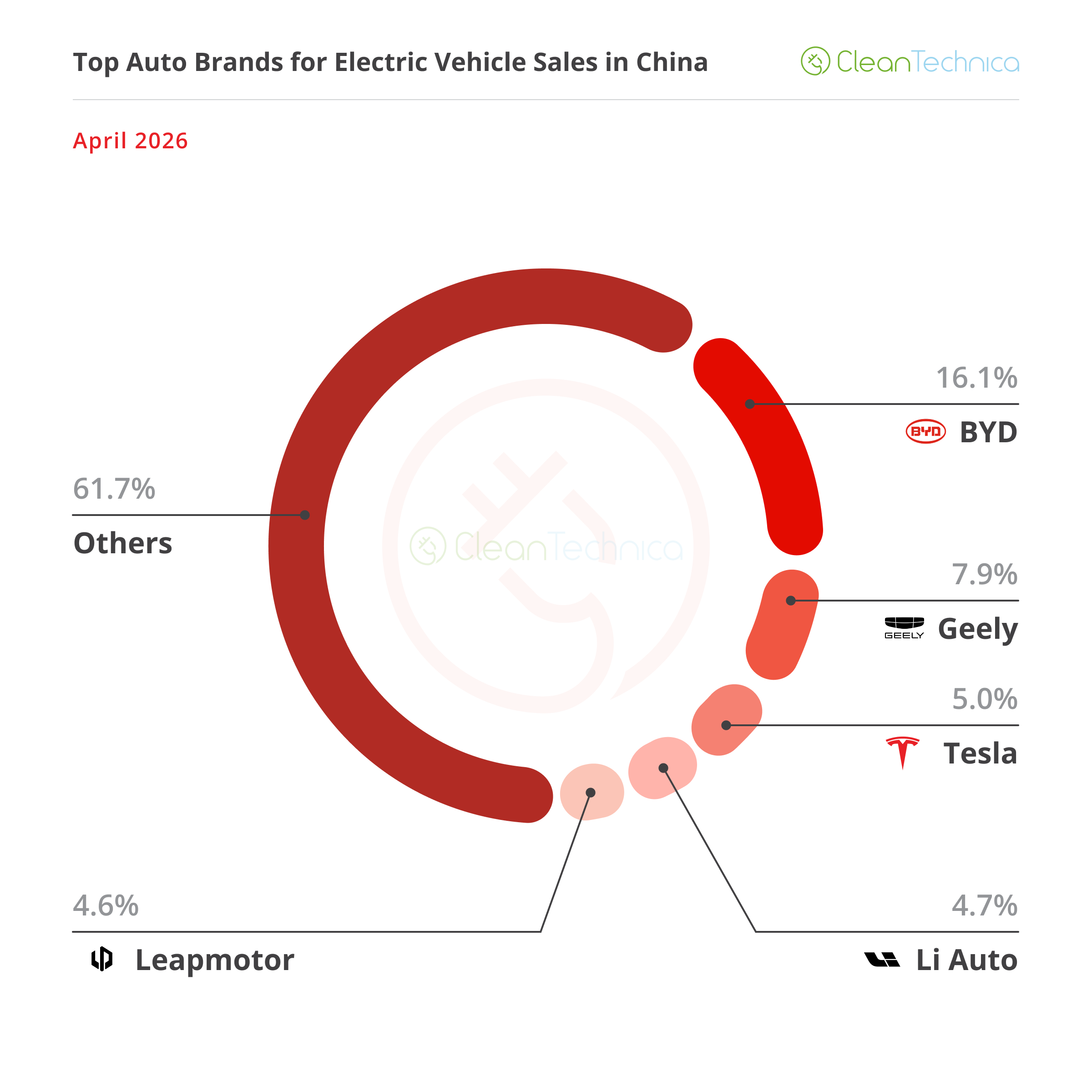

Wanting on the general producer rating, all the pieces appears regular. BYD is on prime, adopted by Geely, Toyota, and Volkswagen.

Solely, it’s removed from being regular. BYD gross sales had been (once more) down 38% YoY. That 2nd era of the Blade battery can’t come quickly sufficient….

And 6 of the highest 10 manufacturers skilled 20%-plus losses, with Volkswagen even crashing 47% YoY!

So, if the massive boys on prime are bleeding gross sales, who’s profitable?

Reply: Startups. #5 Leapmotor was up 102% YoY, to 57,162 registrations, all due to the A10’s success. At #8, Xiaomi can also be rising, up 28%. Lastly, Li Auto. It was #10 in April, and regardless of its gross sales being flat, when everybody else is crashing … you win.

Wanting on the auto model rating, there’s loads of information. Chief BYD (16.1%, up from 15.8%) is gaining floor over runner-up Geely (7.9%, down 0.4%).

Tesla (5%, down from 5.9% in March) held regular in third, however now has 4th positioned Li Auto (4.7%) shut. In the meantime, Leapmotor climbed to fifth, benefiting from Wuling being kicked off the desk.

Under the highest 5, the spotlight is Xiaomi (4.2%, up 0.1%), now in seventh place. Will the startup be capable of rejoin the desk within the coming months?

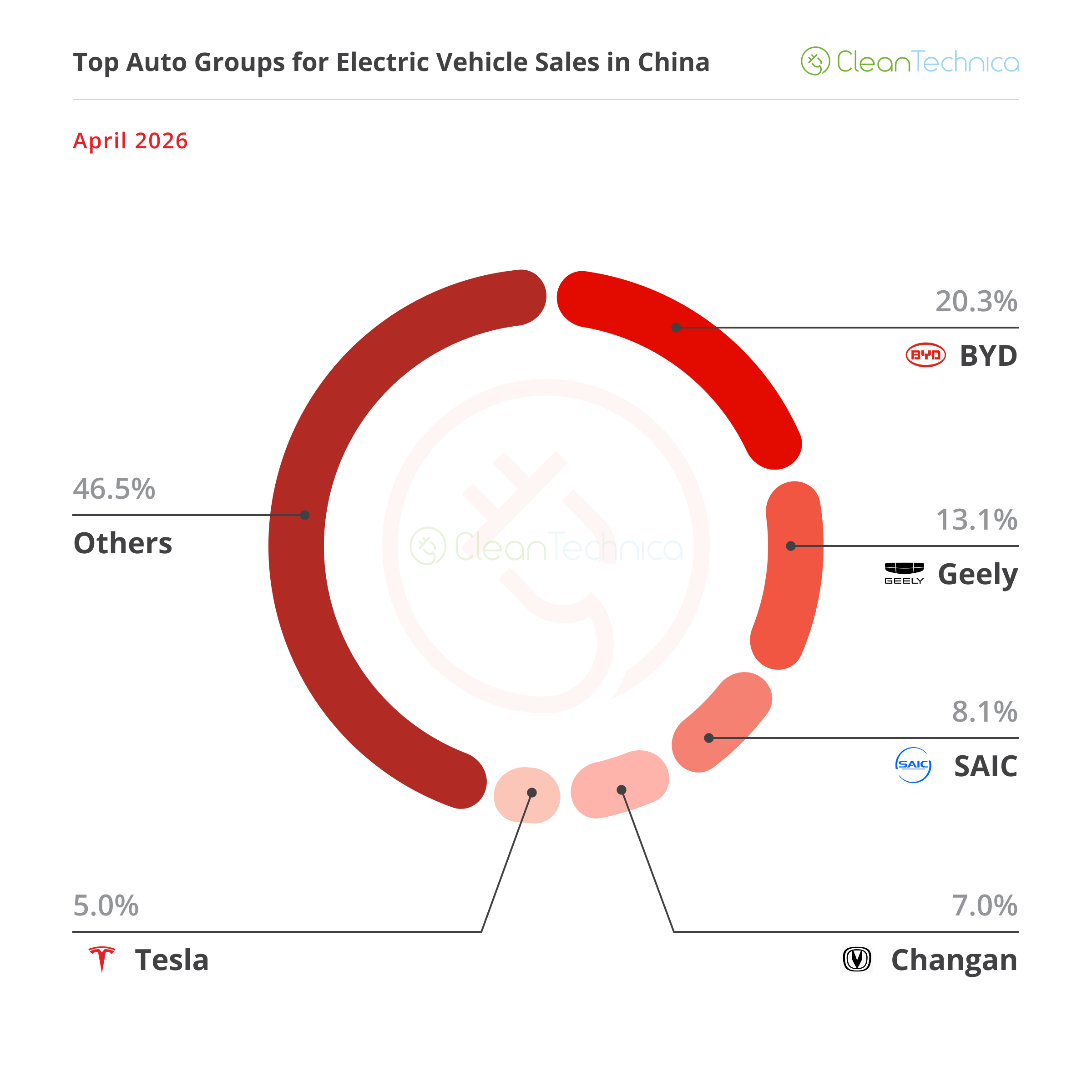

Taking a look at OEMs/automotive teams/alliances, BYD is main, with 20.3% share of the market. It’s up 0.5% in comparison with the earlier month, not solely due to the namesake model, but additionally due to its premium arm, Fang Cheng Bao, which was up 111% YoY in April. In the meantime, #2 Geely misplaced 0.8% share and bought all the way down to 13.1%, seeing BYD put extra distance between it within the race for #1.

Removed from runner-up Geely, #3 SAIC (8.1%) continued to slip, as most of its manufacturers continued within the sluggish lane.

With a rising Changan (7%, up 0.3%) closing in, it wouldn’t be stunning if Chongqing may attain the rostrum subsequent month, or by June.

Lastly, Tesla stayed within the prime 5, in fifth, with 5% share. However with #6 Li Auto (4.7%) and #7 Leapmotor (4.6%) shut by, the Texan should sweat to be able to preserve it’s prime 5 spot.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our every day publication, and comply with us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day publication for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage