Help CleanTechnica’s work by way of a Substack subscription or on Stripe.

Or help our Kickstarter marketing campaign!

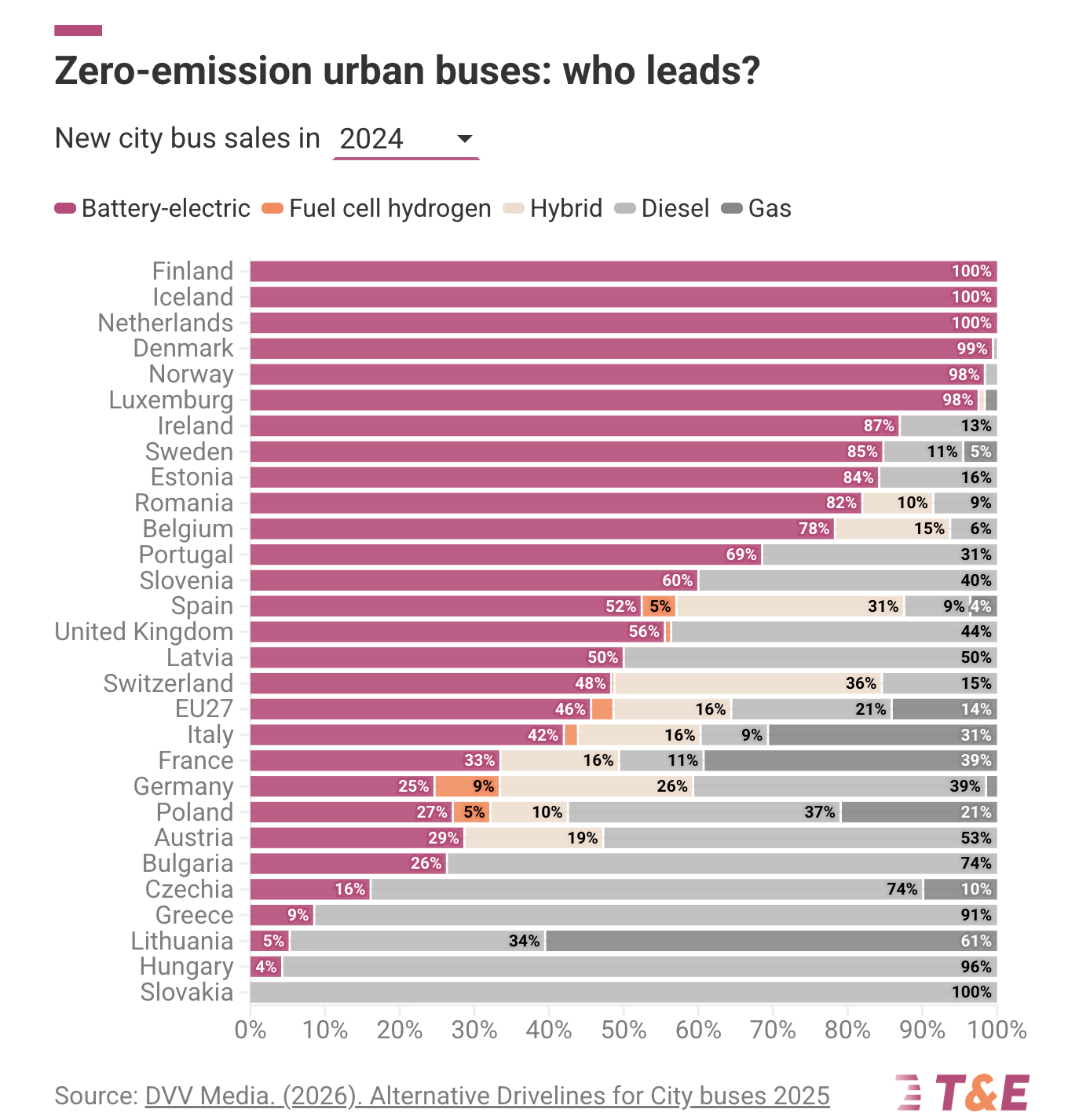

Transport & Setting’s newest European metropolis bus market report glossed in an article in CleanTechnica caught my consideration for a motive that will not be apparent at first look. Battery-electric buses now dominate new metropolis bus registrations throughout the EU, and vastly forward of schedule. That’s the headline, and there’s rather a lot to rejoice with that. However buried within the nation breakdown is one thing that appears contradictory. Germany continues to be at roughly 9% gas cell bus share in 2024 and 2025. The EU as an entire is round 4%. As hydrogen buses have struggled on value, reliability, and infrastructure complexity, why are so many nonetheless showing within the information? The reply lies in denominators, procurement lag, and one very massive nation clearing a backlog of choices made two to 3 years in the past.

Begin with the regulation of small numbers. Slovenia seems within the T&E chart as a hanging outlier in 2025, with hydrogen making up a big share of its purchases. However Slovenia’s complete bus market is small. If a rustic buys 30 metropolis buses in a 12 months and 20 of them are hydrogen, that’s 67%. If it buys 15 and 10 are hydrogen, that can also be 67%. If it buys six and 4 are hydrogen, that’s 67% too. A handful of autos can swing percentages dramatically. With out taking a look at absolute volumes, the chart can suggest a surge that doesn’t exist in actual phrases. Slovenia is a helpful reminder that percentages with out denominators distort notion. The underlying absolute numbers are in a proprietary T&E information set and presumably of their €550 report that I selected to not buy. A publicly obtainable chart of absolute numbers by nation would have been a helpful addition.

Now transfer to the Netherlands, which gives a clearer case research as a result of volumes are significant and coverage is specific. Within the early 2020s, the Netherlands had hydrogen shares approaching 20% in some years. It was an early chief in zero-emission buses and experimented with each battery-electric and gas cell fleets. It constructed refueling depots and deployed hydrogen buses in a number of concessions. Then fleet expertise amassed. Reliability challenges, refueling logistics, and excessive working prices grew to become evident. One area decommissioned its hydrogen fleet and refueling totally. A number of Dutch transit authorities publicly acknowledged that future procurement could be battery-electric solely. The Netherlands is now successfully at 100% zero-emission in new bus tenders, and people zero-emission buses are clearly acknowledged as battery-electric.

But in 2025, the Netherlands nonetheless exhibits roughly 4% gas cell buses in T&E’s dataset. That appears inconsistent with company statements. If the nation registered about 1,090 new buses in 2025 and 4% had been hydrogen, that suggests roughly 44 gas cell buses. That quantity is in step with residual deliveries from awards made in 2023 or earlier, plus concession transfers and administrative re-registrations of current hydrogen fleets. Concession paperwork from 2023 and 2024 required new operators to take over current hydrogen buses and refueling belongings. If a concession adjustments fingers and 20 hydrogen buses transfer between operators, registration information can replicate that motion within the 12 months of switch. It’s potential that’s exhibiting up as an artifact skewing T&E’s information set. The Netherlands gives a clear narrative arc. It moved from roughly 20% hydrogen share throughout early enthusiasm to battery-electric dominance after fleet expertise. The remaining 4% in 2025 is a tail, not a pivot again to hydrogen.

On the EU stage, the numbers are skewed by Germany. Germany is the most important metropolis bus market within the EU and the most important hydrogen bus market. If Germany is at 9% gas cell share in and sells 1,200 metropolis buses in a 12 months—my finest estimate from the general public information obtainable to me—, that’s round 108 hydrogen buses, in step with earlier years’ anouncement. Smaller international locations can present increased percentages, however their volumes are too low to maneuver the EU combination. Germany’s 9% is what holds the EU common round 4%. Take away Germany from the equation and the EU hydrogen share would fall sharply.

The information for 2024 registered gas cell buses in Germany is revealing. 9% of buses the place hydrogen electrical in that 12 months, with solely 25% battery electrical buses being registered. Between 2024 and 2025, battery electrical leapt as much as 41%, whereas hydrogen plateaued at 9%. Germany clearly beginning determining that battery electrical was the successful drive prepare through the procurement window that led to 2025 deliveries.

The important thing query is whether or not Germany’s 9% is a gentle state or a trailing indicator. Publicly seen procurement information suggests the latter. In 2022 and 2023, there was a wave of hydrogen bus awards throughout Germany. DB Regio Bus introduced a framework masking 60 hydrogen buses in early 2023. Rebus Rostock ordered 52 hydrogen buses in 2023, supported by federal funding. Duisburg’s DVG awarded a contract for 25 hydrogen buses in mid-2023, with deliveries extending into 2025. Krefeld and different operators positioned orders within the 10 to 30 bus vary. Add these collectively and 2023 alone accounts for nicely over 130 hydrogen buses from a handful of huge patrons.

| Yr | Operator / Area | Buses | OEM | Announcement Yr | Said Supply Window |

|---|---|---|---|---|---|

| 2023 | DB Regio Bus | 60 | CaetanoBus / Toyota | 2023 | Deliveries starting 2024 onward |

| 2023 | Rebus Rostock (Mecklenburg-Vorpommern) | 52 | Solaris | 2023 | Delivered by way of 2024–early 2025 |

| 2023 | DVG Duisburg (NRW) | 25 | Solaris | July 2023 | 12m buses 2024, articulated mid-2025 |

| 2023 | SWK Mobil Krefeld (NRW) | ~15 | Solaris | Oct 2023 | Deliveries by way of Could 2025 |

| 2024 | Ruhrbahn Essen (NRW) | 19 | Solaris | Jan 2024 | Deliveries 2024–2025 |

| 2024 | REVG Kerpen (NRW) | 26 | Solaris | Aug 2024 | Remaining deliveries in 2025 |

| 2024 | RVK Cologne Area (NRW) | 20 agency (+20 choice) | Solaris | Mar 2024 | Deliveries starting 2024, extending into 2025 |

| 2024 | Cottbus / Spree-Neiße | 46 | Wrightbus | Apr 2024 | Gradual deployment in 2025 |

| 2024 | Saarbahn Saarbrücken | 28 | Wrightbus | 2024 | Deliveries beginning 2024 |

| 2024 | Rheinbahn Düsseldorf (NRW) | 10 | Solaris | 2024 | Supply in 2025 |

| 2024 | LNVG Groß-Gerau (Hesse) | 23 | Solaris | Jan 2024 | Articulated models mid-2025 |

| 2025 | WestVerkehr (NRW) | 12 | Wrightbus | 2025 reporting | Deliveries in 2025 (order secured earlier) |

Bulletins of EU gas cell bus awards by creator

These 2023 awards translated into 2024 and 2025 deliveries. Duisburg’s buses entered service in 2024 and 2025. Rostock’s fleet was integrated into operations by early 2025. These deliveries seem in 2024 and 2025 registration information, reinforcing the 9% share. However they’re the end result of choices made when hydrogen enthusiasm and federal help had been at a excessive level.

In 2024, hydrogen awards didn’t disappear. Ruhrbahn in Essen ordered 19 hydrogen buses in early 2024 with deliveries scheduled by way of 2025. REVG Kerpen ordered 26 hydrogen buses in 2024 with deliveries extending into 2025. RVK within the Cologne area expanded its hydrogen fleet once more in 2024. Cottbus and Saarbrücken introduced hydrogen orders from Wrightbus in 2024, together with batches of 28 and 46 buses. Even a conservative tally of publicly seen 2024 awards reaches nicely over 120 buses. That doesn’t seem like a collapse 12 months. It seems to be just like the final robust 12 months of ordering.

The 2025 image is totally different. Publicly seen new hydrogen bus awards in 2025 are nearly nonexistent in contrast with 2024. The one instance I may discover is WestVerkehr’s order of 12 hydrogen buses, however that order traces again to commitments made in 2024 and at the least some deliveries reported in 2025. That doesn’t show that orders have fallen off a cliff, but it surely strongly suggests it. Cities proceed to announce awards for battery electrical fleets, and there’s no proof of abatement of that. T&E ought to try to mission the trajectory’s of buses. They’ve proprietary information units and entry to information that might allow them to do the evaluation.

Procurement timelines matter. A typical cycle runs from funding approval to tender publication to award to supply over 18 to 30 months. If enthusiasm and funding peaked in 2022 and 2023, awards would cluster in 2023 and 2024. Deliveries and registrations would cluster in 2024 and 2025. If new awards sluggish in 2025, the affect wouldn’t present up in registration shares till 2026 and 2027. The 9% hydrogen share in Germany in 2024 and 2025 could be in step with a slowdown in new awards, as a result of it displays earlier choices working by way of the system.

Germany could have the longest and largest hangover as a result of it positioned the most important orders. If Germany awarded roughly 130 hydrogen buses in 2023 and one other 120 or extra in 2024 amongst main operators, that’s over 250 buses feeding into 2024 and 2025 deliveries. Even when 2025 awards fall to some dozen nationwide, the supply pipeline will take time to empty. The 9% plateau might symbolize the crest of deliveries reasonably than the crest of enthusiasm.

The Netherlands gives a glimpse of what comes subsequent. It examined hydrogen at scale, reached double-digit shares, after which pivoted to battery-electric solely tenders after accumulating operational expertise. Its 2025 hydrogen share seems to be the residual tail of earlier awards and concession re-registration mechanics. Germany is on a bigger scale and has deeper hydrogen ecosystem commitments, so the tail will probably be longer. However even in Germany, hydrogen stays below 10% of latest metropolis bus registrations and has seemingly peaked. It’s not a dominant expertise. It’s a minority expertise clearing a backlog of choices made in a unique coverage second. Germany will undoubtedly observe within the Netherlands tire tracks, with companies asserting extra fleet abandonments, refueling decommissioning and doubling down on battery electrical.

Arguably, Germany’s ongoing Gruppendenken round hydrogen has contributed to there poor rating when it comes to buying battery electrical buses. When they’re solely at 41% and different main European international locations are at 75% and better, they’re distinctly lagging, and hydrogen buses suck of procurement cycles, cash and energy that might have gone rather a lot additional with battery electrical buses.

If publicly seen hydrogen bus awards in Germany stay low in 2025 and 2026, the registration information in 2026 and 2027 will seemingly replicate that. The EU is already at peak gas cell bus deliveries in my view primarily based on this evaluation. The present plateau is the final excessive level earlier than decline, pushed by the lengthy procurement lag between political enthusiasm and autos getting into service.

Help CleanTechnica by way of Kickstarter

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our day by day publication, and observe us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our day by day publication for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if day by day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage