Help CleanTechnica’s work by means of a Substack subscription or on Stripe.

Aberdeen’s determination to retire and attempt to promote its 25 hydrogen double decker buses closes a chapter that started with assured claims about international management in clear transport. The fleet was promoted because the world’s first hydrogen double deck operation and positioned as a basis for a broader hydrogen economic system that may anchor a whole lot of native jobs. After a number of years of blended efficiency, infrastructure pressure, and parallel deployment of battery electrical buses, the council selected to pivot away from hydrogen. The choice was in all probability cathartic for a lot of in Aberdeen. It was arithmetic catching up with ambition.

The council has indicated that it intends to promote the 25 hydrogen double deckers to get better some capital, however the probability of reaching a significant resale worth is low. There is no such thing as a deep or liquid secondary marketplace for used hydrogen buses. Earlier hydrogen bus pilots in locations comparable to British Columbia ended with autos being listed on the market, but these instances didn’t result in the emergence of an ongoing aftermarket. Hydrogen buses are tightly coupled to particular refuelling infrastructure, upkeep experience, and provide contracts, which sharply limits the pool of potential patrons. Any operator contemplating a used hydrogen bus should have already got suitable hydrogen provide and educated technicians, or be prepared to construct that functionality for a small fleet of ageing autos. In apply, most hydrogen deployments have been grant-supported pilots fairly than commercially scaled programs, so the variety of potential purchasers is small. Aberdeen might discover a purchaser, however the expectation of a considerable capital restoration is optimistic given the absence of a functioning international resale market.

If the main target is strictly on hydrogen double deck buses, the used market is skinny. The first platform in operation has been the Wrightbus StreetDeck Hydroliner, deployed in restricted numbers in London, Aberdeen, and Northern Eire. London launched an preliminary batch—doubtless as a consequence of political stress from hydrogen-focused Lord Bamford, founding father of JCB, to maintain his son’s firm WrightBus out of insolvency—however has not pursued follow-on orders, as a substitute concentrating new procurement on battery electrical double deckers. Belfast and Metrobus added some extra hydrogen items, however these stay small fleets fairly than quickly scaling applications. There is no such thing as a proof of a broad procurement wave of hydrogen double deck buses throughout the UK akin to the regular and far bigger rollout of battery electrical double deckers in main cities. The know-how persists solely in area of interest deployments, with no development momentum that may recommend prepared patrons.

The unique imaginative and prescient was coherent inside the misguided optimism of the mid 2010s. Hydrogen was broadly framed as a common power service. Scotland was in search of post-oil positioning, and like many fossil gas economies noticed hydrogen as an power carrying savior. Aberdeen had already invested in hydrogen infrastructure, together with the Kittybrewster refuelling station delivered in 2015 at roughly £1 million in capital from BOC. By 2020, 15 hydrogen double deckers had been delivered below an £8.3 million program supported by the Scottish Authorities and EU funding. Ten extra adopted below an extra £4.5 million award. Particular person buses had been round £500,000 every. The plan was that this fleet would anchor a hydrogen hub, scale into heavy autos, and assist justify new native hydrogen manufacturing.

The economics of the refuelling station had been at all times the important issue. Kittybrewster was designed for about 360 kg of hydrogen per day, or roughly 131,400 kg per 12 months at full utilization. Reported throughput suggests about 160 tons disbursed over 4 years, which works out to round 40,000 kg per 12 months. That’s about 30% of nameplate capability. The 2024 council documentation recorded working prices of roughly £974,000 over three years, or roughly £325,000 per 12 months. In opposition to a £1 million capital value, that’s about 30% of capex yearly in O&M alone. That aligns with what I’ve beforehand calculated for California hydrogen refuelling stations, the place O&M regularly lands within the 20% to 35% of capex per 12 months vary as soon as compressors, service contracts, and staffing are included. It doesn’t align with the 4% O&M assumptions nonetheless embedded in lots of transportation value fashions and is one other information level concerning the excessive value of operating hydrogen refueling stations.

The distinction with battery electrical charging infrastructure is structural. A hydrogen refuelling station comparable to Kittybrewster is successfully a small industrial plant, with electrolysers which have finite stack life, excessive stress compressors, drying programs, storage vessels, security programs, and specialised dispensers. Electrolyser stacks usually require main refurbishment inside a decade, compressors are upkeep intensive, and O&M can run within the 20% to 35% of capex per 12 months vary, as Aberdeen’s personal numbers point out. By comparability, a battery electrical depot charging set up is primarily electrical infrastructure: grid connection upgrades, transformers, switchgear, rectifiers, and charging cupboards. There is no such thing as a gas manufacturing, no excessive stress storage, and no chemical processing. Upkeep is usually a small fraction of capex, there aren’t any stacks to switch and no compressors to overtake, and enlargement is modular and incremental as fleets develop. When a charging unit reaches finish of life it’s changed as a element. When a hydrogen station reaches finish of life it usually requires coordinated and capital intensive reinvestment throughout a number of subsystems. That distinction in complexity and lifecycle burden goes a good distance towards explaining why one struggled to justify additional capital and the opposite scales predictably with demand.

Annualizing the £1 million capital funding over 10 years at a 7% company low cost fee yields about £142,000 per 12 months. Including the recorded £325,000 per 12 months in O&M brings fastened annual value to roughly £467,000. At 40,000 kg per 12 months, fastened value alone is about £11.70 per kg. Even when throughput had been nearer to 60,000 kg per 12 months, fastened value would nonetheless be round £7.70 per kg. Full system electrical energy consumption for onsite electrolysis together with stability of plant and compression is about 65 kWh per kg. Utilizing a sensible giant enterprise electrical energy fee in Scotland of roughly £0.205 per kWh, electrical energy alone prices about £13 per kg. Including fastened value produces hydrogen within the vary of roughly £20 to £25 per kg at Kittybrewster.

The hydrogen refuelling station didn’t fail due to some single dramatic breakdown however as a result of it reached the sensible finish of its preliminary operational life and required substantial reinvestment to proceed working. Kittybrewster was exhibiting its age by the early 2020s: compressors, dispensers and the electrolysis stacks themselves had been approaching the purpose at which main overhauls or replacements are typical in hydrogen station life-cycle plans, and the station had delivered solely a fraction of its theoretical throughput as a result of the fleet itself by no means created the sustained demand foreseen in early venture fashions.

Council papers in 2024 laid out {that a} life-extension programme was wanted to maintain the station in service, however BOC, because the proprietor and operator, declined to spend money on that capex with out long-term contractual ensures on operations and income from the council or its companions. From BOC’s perspective this was a enterprise determination: and not using a agency dedicated offtake or long-term working contract to underwrite the price of stack substitute, compressor servicing and controls upgrades that may doubtless run into the low a whole lot of hundreds of kilos, the danger and price had been theirs to hold for unsure future profit. Because the working contract expired, BOC started decommissioning actions, and the station stopped common manufacturing, leaving the hydrogen buses successfully stranded with out dependable gas. This sequence of reaching end-of-life technical necessities, absence of a transparent income stream to justify overhaul prices, and the station ceasing to supply gas set the stage for the council’s pivot away from hydrogen altogether.

The council thought-about taking possession of the asset. Council papers in 2024 point out that officers had been exploring a switch in order that public funds may very well be used to refurbish and prolong the station’s life, fairly than investing in a privately owned facility. The logic was that if hydrogen remained a part of Aberdeen’s transport technique, the town would want direct management over its refuelling infrastructure. In apply, this may have meant the council assuming not simply the capital value of upgrades however the ongoing technical and monetary danger of working a small, under-utilized hydrogen plant.

By the point the council formally determined to eliminate the fleet, the hydrogen buses had already been successfully sidelined for a chronic interval. Reporting signifies that common service ceased in mid to late 2024 as refuelling reliability deteriorated and manufacturing on the Kittybrewster station faltered. Meaning the buses sat idle for effectively over a 12 months earlier than the ultimate coverage pivot in early 2026. For a capital asset designed round a 15-year service life and roughly 1,000,000 km of operation, dropping 12 to 18 months of lively deployment is just not a minor disruption. It represents a significant erosion of anticipated lifetime utilization and additional worsens the already strained value per km economics.

The broader hydrogen technique in Aberdeen was tied to a bigger plan for expanded refuelling capability below a three way partnership with BP, structured by means of an organization known as bp Aberdeen Hydrogen Power Restricted. That venture had moved effectively past conceptual levels: the council authorized seed funding, planning permission was granted for a brand new hydrogen manufacturing and refuelling facility at Hareness Street linked to a photo voltaic farm on the previous Ness landfill, and a phased construct was envisaged that may produce over 800 kg of hydrogen per day in its first part with capability to develop to a number of tonnes as demand expanded.

The narrative supporting that plan rested on the idea that the town’s personal hydrogen double-deck fleet and different future hydrogen autos would create predictable demand, justifying each the capital funding and the long-term working commitments. Kittybrewster was part one, BP’s facility was supposed to switch it as part 2 and there have been expectations of a part 3 with transport and aviation fuels. With the collapse of hydrogen as a viable bus resolution and no different giant, dedicated offtake on the horizon, the council is now actively in search of to unwind or exit its obligations within the three way partnership fairly than proceed with constructing out the hub. What was as soon as offered as an financial alternative and regional anchor venture has develop into a legal responsibility of unsure worth exactly as a result of the foundational demand assumptions have evaporated.

Aberdeen Metropolis Council faces actual monetary and contractual publicity because it seeks to unwind its three way partnership with BP over the deliberate hydrogen manufacturing hub, which had been budgeted at round £20 million for the primary part of build-out. Officers are understood to be in negotiations on methods to switch or terminate the partnership fairly than merely stroll away, which might contain bearing prices tied to planning, website preparation, allowing and early venture growth that BP and the council had already dedicated to below the three way partnership settlement.

As a result of BP made a remaining funding determination in mid-2024 and the enterprise had progressed towards building earlier than being paused, the council can also want to deal with sunk prices it agreed to below JV funding preparations in addition to any liabilities for commitments made to 3rd events or contractors. In discussions reported between the council and BP, a part of the exit planning seems to contain negotiating the switch of the three way partnership entity again to the council in order that property and obligations will be managed in a means that aligns with the pivot to battery electrical infrastructure, however this switch itself is more likely to carry accounting and money implications for Aberdeen’s stability sheet and future capital programmes.

This set of ongoing fiscal liabilities after the top of makes an attempt to develop hydrogen fleets is typical as effectively. My steering piece for transit businesses anticipating to obtain hydrogen buses round a danger mitigation workshop makes it clear that cities and businesses have to rigorously plan for failure to keep away from being left on the hook.

It is usually value remembering that the hydrogen double deck fleet was not Aberdeen’s first try at hydrogen buses. Between 2015 and about 2020 the town operated ten Van Hool A330H single deck hydrogen buses as a part of the unique Aberdeen Hydrogen Bus Mission. These autos had been fuelled on the Kittybrewster station and ran in common service for roughly 5 years below a publicly funded demonstration program. When that part ended, the buses had been withdrawn fairly than forming the muse of a rising business fleet. A minimum of one entered museum preservation, and there’s no proof of a significant secondary market or redeployment elsewhere. In different phrases, Aberdeen had already accomplished a full hydrogen bus trial with Van Hool single deckers earlier than committing to 25 new double deckers. These buses value about €850,00, vastly greater than any buses, however had been apparently absolutely funded by the EU Jive program earlier than being deserted. One went right into a museum and the remainder apparently had been scrapped. The second part was not a primary experiment. It was a renewed guess on a know-how that had already been examined domestically and had not scaled organically.

As a reminder, Van Hool was one of many early European producers to make a big strategic guess on hydrogen gas cell buses, positioning fashions such because the A330H as a part of a zero-emission future effectively earlier than battery electrical buses had matured. That guess coincided with different strategic strains, together with aggressive enlargement, publicity to low-margin contracts, and provide chain disruptions within the early 2020s. By 2024 the corporate entered chapter proceedings, and its property had been cut up between new homeowners, with the bus division successfully carved up fairly than persevering with as a unified producer. The hydrogen focus was not the only explanation for its collapse, however it was a part of a portfolio of high-risk bets in a market that shifted quickly towards battery electrical. On the similar time, Dutch transit authorities that had as soon as explored hydrogen for regional buses more and more pivoted to battery electrical fleets, citing value, infrastructure simplicity, and reliability. The Netherlands, lengthy thought-about open to hydrogen in mobility, has in apply moved decisively towards electrification for city and regional bus transit, reinforcing the broader European pattern away from hydrogen buses at scale.

Van Hool is way from alone in OEMs which have dedicated to hydrogen drive trains coming into insolvency. The variety of entrants which nonetheless supply hydrogen autos is overtopped by those which have exited the market or gone bankrupt. Quantron, Nikola and Hyzon are greater profile failures, however removed from the one ones.

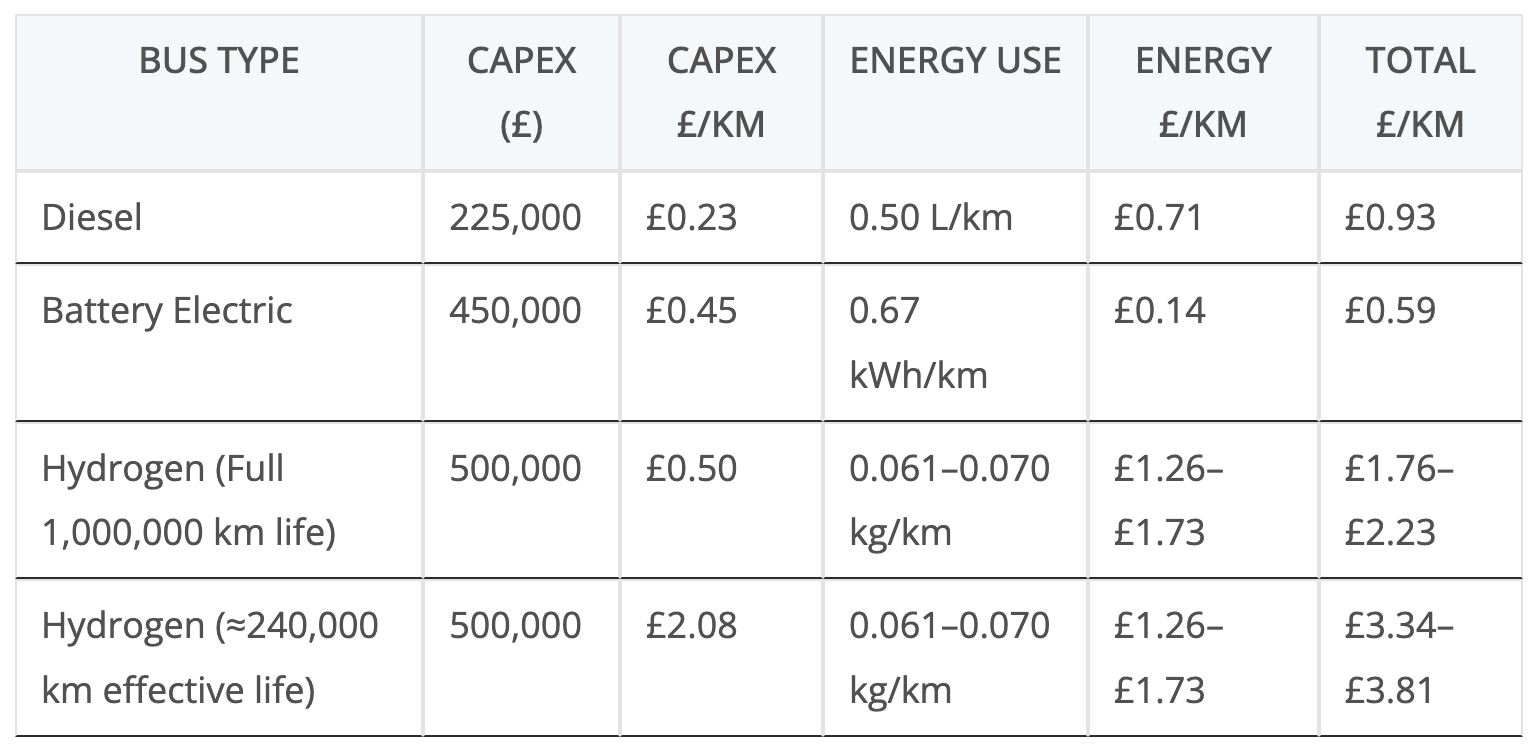

When translated into value per kilometre, the image turns into clearer. Hydrogen double deck buses usually devour about 6 to 7 kg per 100 km, or 0.06 to 0.07 kg per km. At £22 per kg midpoint, that’s round £1.32 to £1.54 per km in power. Utilizing the higher finish of the fee vary pushes that to round £1.70 per km. Diesel double deckers usually devour about 0.5 litres per km. At roughly £1.42 per litre, gas value is round £0.71 per km. Battery electrical double deckers such because the Enviro400EV devour about 0.67 kWh per km. At £0.205 per kWh, electrical energy value is about £0.14 per km. On power alone, hydrogen is roughly 2 to 4 instances the price of diesel and about 10 instances the price of battery electrical in Aberdeen’s context.

Taking a look at full lifetime capital and power prices reinforces the hole. Assuming a 1,000,000 km service life, capital value per km for a £500,000 hydrogen bus is £0.50 per km. Diesel buses at roughly £225,000 land at about £0.23 per km. Battery electrical buses at round £450,000 are about £0.45 per km. Including power value produces totals of roughly £0.93 per km for diesel, about £0.59 per km for battery electrical, and between £1.76 and £2.23 per km for hydrogen.

Nonetheless, the Aberdeen hydrogen buses didn’t obtain something near a full design life. In the event that they successfully delivered on the order of 240,000 km earlier than being sidelined, capital value alone rises to about £2.08 per km, pushing whole value into the £3.34 to £3.81 per km vary earlier than upkeep and infrastructure are thought-about. This type of foreshortened life is just not uncommon in hydrogen bus trials globally, the place reliability, refuelling constraints, and coverage pivots usually stop fleets from reaching their theoretical lifetime. Even below beneficiant full-life assumptions hydrogen struggles to compete. Below real-world outcomes, the economics deteriorate additional.

Infrastructure scale compounded the danger. Hydrogen stations are dominated by fastened value. Low utilization drives up value per kg. Kittybrewster was operating at roughly 30% of capability. The proposed BP hydrogen hub was designed to supply greater than 800 kg per day in its first part, greater than double Kittybrewster’s capability. That enlargement assumed development in hydrogen autos. As a substitute, hydrogen heavy autos didn’t scale in significant numbers. The bus fleet remained the first demand anchor. Scaling provide with out scaling demand will increase monetary publicity. The mathematics doesn’t enhance as a result of coverage hopes it is going to.

Operational complexity added additional friction. First Aberdeen was managing diesel, battery electrical, and hydrogen buses in the identical depot setting. Every drivetrain requires completely different abilities, instruments, elements, and security procedures. Hydrogen provides excessive stress storage, gas cell stacks, and extra cooling programs. Within the steering I ready for a hydrogen danger mitigation workshop for transit businesses, I explicitly really helpful retaining diesel buses previous their anticipated finish of life as contingency cowl for hydrogen reliability points. Aberdeen successfully adopted that sample, borrowing diesel buses when hydrogen items had been withdrawn. Sustaining three drivetrain applied sciences will increase value and complexity. It doesn’t make failure inevitable, however it reduces resilience.

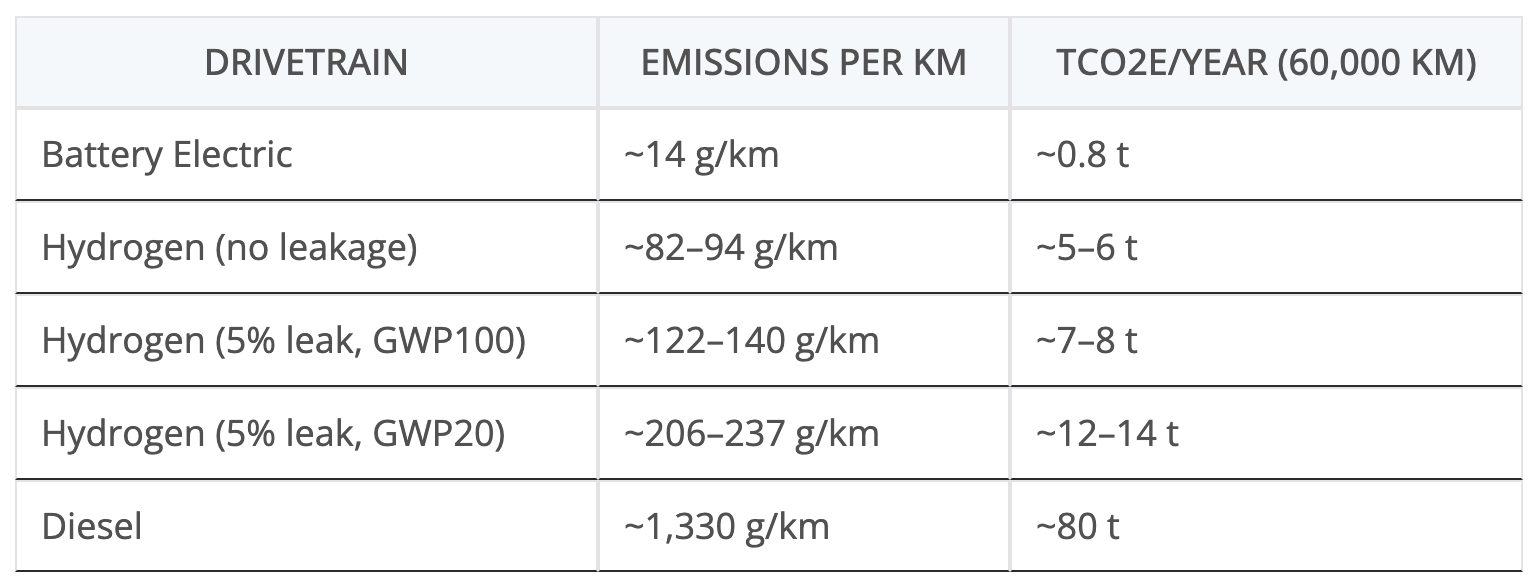

On operational emissions alone, the distinction between the three drivetrains is stark even on Scotland’s comparatively clear grid. Utilizing Scotland’s common electrical energy carbon depth of about 20.7 gCO2e/kWh, a battery electrical double deck consuming roughly 0.67 kWh/km emits about 14 gCO2e per km, or about 0.8 tCO2e per 12 months at 60,000 km. A diesel double deck consuming about 0.5 litres per km at 2.66 kgCO2e per litre emits roughly 1.33 kgCO2e per km, which is near 80 tCO2e per 12 months over the identical distance. A hydrogen bus equipped by onsite electrolysis utilizing about 65 kWh/kg and consuming 6.1 to 7.0 kg per 100 km lands round 5 to six tCO2e per 12 months on a no-leakage foundation. Nonetheless, assuming 5% hydrogen leakage, an inexpensive assumption based mostly on leakage information from hydrogen infrastructure leakage research, and making use of a GWP20 of about 37, whole operational affect rises to roughly 12 to 14 tCO2e per 12 months. Even on a low-carbon grid, hydrogen sits an order of magnitude above battery electrical and much under diesel, however leakage meaningfully narrows the hole.

This consequence is just not remoted. Brussels deserted its hydrogen bus trial after confronting excessive gas value and provide challenges. Whistler deserted its fleet as quickly because it might, 4 years in. A number of different European hydrogen bus applications have scaled again or pivoted to battery electrical. Within the UK, hydrogen fleets have struggled with availability and refuelling reliability. Beijing’s Winter Olympic hydrogen refueling stations and bus fleet are more and more fenced off, parked and infiltrated with vegetation. Globally, hydrogen bus deployments have plateaued whereas battery electrical bus registrations proceed to develop. The sample is seen throughout jurisdictions.

The predictability rests on power conversion physics. Hydrogen for buses requires electrical energy to run electrolysis at roughly 65% effectivity. Compression and storage add extra losses. Gas cells convert hydrogen again into electrical energy at roughly 50% to 60% effectivity. The general spherical journey from grid to wheels is usually under 35%. Battery electrical buses transfer electrical energy from grid to wheels at above 80% effectivity. Every extra conversion step provides value. When electrical energy costs are excessive, these losses are magnified.

Aberdeen had entry to those numbers earlier than the buses had been bought. That they had already trialed hydrogen buses and refueled them. The associated fee construction of hydrogen refuelling stations was not hidden. O&M burdens effectively above 20% of capex per 12 months had been seen in California and different markets, along with their very own expertise. A number of hydrogen bus trials had already struggled or been curtailed globally. The selection to proceed was a deliberate coverage determination. The one unambiguous optimistic growth on this story is the choice to retire the hydrogen bus fleet and pivot to battery electrical. It’s applicable to acknowledge the correction, not the preliminary error.

The broader lesson is easy. City buses are an electron drawback. They function on fastened routes, return to depots nightly, and might cost on predictable schedules. In movement charging is easy and solves key route and elevation issues. Hydrogen has roles in fertilizer manufacturing, refining, and sure industrial warmth purposes the place molecules are required. Utilizing hydrogen for city buses competes immediately with battery electrical programs which can be easier and cheaper. When the power value distinction exceeds £1 per km, subsidies can delay adjustment however can not shut the hole.

All required pilot initiatives have already been carried out. Aberdeen ran one. Brussels ran one. California ran many. The outcomes converge. Excessive fastened infrastructure value, excessive O&M, low utilization, costly gas, and eventual transition to battery electrical. Demonstrations are precious when uncertainty is excessive. On this case, uncertainty has been changed by repetition. The power transition might be formed by applied sciences that scale economically, not by applied sciences that require persistent subsidy to compete.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our every day publication, and observe us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day publication for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage