Is Europe Again within the Race? Many New European EVs Might, in Principle, Be Aggressive in Latin America

Assist CleanTechnica’s work by a Substack subscription or on Stripe.

China is the Queen of EVs. That a lot we all know for sure. The benefit that Chinese language automakers have — rightfully — gained over their rivals is not going to be a straightforward one to beat. And but, to take the autumn of the centennial car industries of North America, Europe, and non-Chinese language East Asia with no consideration feels to me like leaping the gun, even when the Chinese language risk is in contrast to something these industries have ever confronted earlier than.

(Discover that I write “Car Industries” as a substitute of “Legacy Auto” as a result of the a part of the business that may stay could nicely not be Legacy Auto, however incumbent native gamers. This I discover notably doubtless in North America.)

One of many perks of residing in a growing nation is that I get to see firsthand the battle between the established gamers and the incumbent Chinese language manufacturers with out the distortions attributable to both the hyper-competitive Chinese language market (with many manufacturers promoting at a loss) or the tariff partitions constructed to guard the native business in North America and the EU. And since 2022, the inevitable conclusion has been that the Chinese language don’t have any peer within the EV sector … however that competitors may, ultimately, come up.

A 12 months in the past, I used to be centered on North America. The US underneath Biden had been aggressively selling native battery manufacturing in addition to built-in provide chains within the larger North American area, making it a really stable manufacturing hub with entry to ample sources, low cost power, and the prowess of Mexico’s business, which, in contrast to the USA’s, can rent expertise at a value even decrease than their Chinese language competitors. Again then, I wrote {that a} window of alternative could possibly be opening for GM, because the just lately introduced Equinox EV was probably the most inexpensive automobile in Latin America with a battery over 80 kWh. However I additionally stated this:

In fact, there are a lot of methods this will likely fail.

[…]

It could be that political will in direction of EVs cools within the US and GM pauses its ramp-up, dropping this small window of alternative to turn out to be aggressive with the Chinese language manufacturers.

Lo and behold, because of President Trump, battery manufacturing within the US is now not booming, power is getting far more costly, and the massive, lovely provide chains by North America have been damaged, maybe irreversibly. Mexico will attempt to compete by itself, and maybe will even succeed, however these days, most attention-grabbing issues are taking place on the opposite facet of the Atlantic.

The wave of inexpensive EVs touchdown on Europe

A 12 months in the past, my optimism was restricted to at least one firm (GM) and one mannequin (the Equinox EV). However in Europe, because of that pesky interference of the EU and its draconian emissions requirements, the upcoming competitors is just not restricted to at least one firm, a lot much less one mannequin.

It was the Renault Twingo E-Tech that made me take into consideration this matter. In response to Latin American media, it is going to boast a 40 kWh battery and have a worth of “underneath €20,000” (taxes included) which — translating into native forex — means underneath R$124.000 in Brazil and COP$90’000.000 in Colombia. And guess what? In case you had been to buy a 38 kWh BYD Seagull in Brazil or Colombia, it could price R$119.000 and COP$85’000.000, respectively. Which means, if imported in Latin America on the similar costs because it’s bought in Europe, the Twingo E-Tech could be a really sturdy competitor towards the BYD Seagull. And simply as vital, this mannequin was allegedly developed in solely two years, which isn’t removed from the hyper-quick growth that characterizes Chinese language manufacturers.

There are others. At lower than €25,000, the upcoming Skoda Epiq may face the marginally bigger BYD Yuan Up (€24,500), whereas the Fiat Grande Panda (apparently bought at round €23,000) may nicely face the BYD Dolphin at roughly the identical worth. I may maintain occurring, but it surely must be clear that even Stellantis (sure, that Stellantis) appears to be a succesful competitor right here.

And one thing I’m but to report on, however that additionally compounds right here, is that the Chevrolet Spark EUV has been a huge success, reaching the highest 5 on its first month in Brazil, Uruguay, and Colombia, and changing into the best-selling EV within the (admittedly minuscule) Argentinian market. The Spark EUV stands roughly on the worth of the BYD Dolphin, but stays dearer than comparable rivals such because the Geely Geometry E or the JAC E30X. Its success proves that individuals right here need EVs and are prepared to pay a small premium to get one from the manufacturers they know and love as a substitute of getting to decide on a wholly new (and unknown) one. This, even when the EV in query is inbuilt China, as is the case of the Spark EUV (which is a rebranded Baojun Yep Plus).

So, there’s no cause why the Spark EUV’s success couldn’t be replicated by the Twingo E-Tech or the Skoda Epiq, solely this time being a European made EV.

Past optimism, a dose of actuality.

Europe’s EV business standing is kind of promising, should you ask me, however please don’t take me as saying Europe has caught up with China. Categorically, it has not.

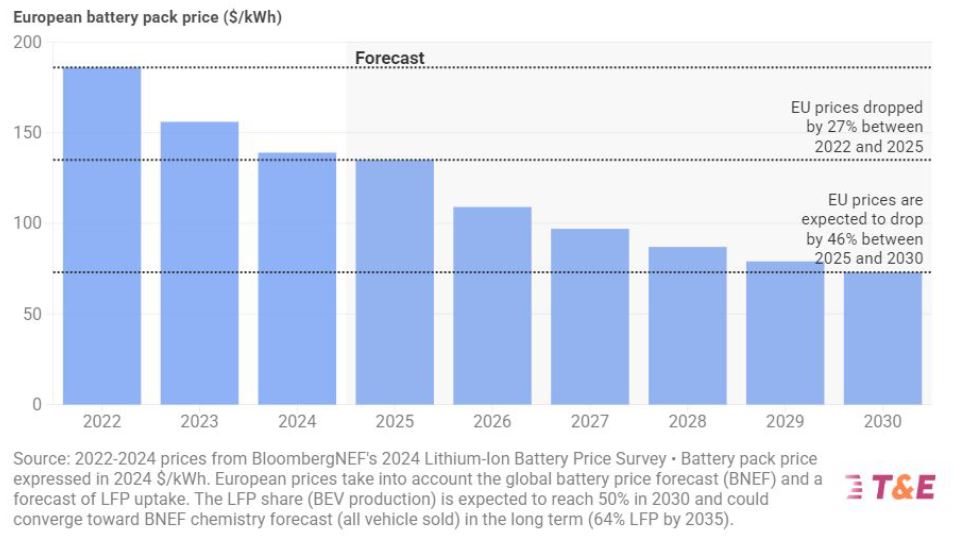

Chinese language EV makers depend on probably the most environment friendly battery provide chain the world has ever seen, with costs as little as $50/kWh this 12 months (although, prone to be barely greater on common). In response to a current report by Transport & Atmosphere, Europe’s battery costs this 12 months stand at virtually thrice that quantity, and by 2030 will solely attain $75/kWh, which means let’s imagine Europe is now 5 years behind China concerning battery prices, and even perhaps extra concerning supplies provide chains.

China has additionally entered a state of hyper-competition that the EU will merely not permit, which means that it’s doubtless innovating sooner and that pricing within the native market is much under export markets, so ought to the necessity come up, they’ll simply lower costs abroad. This additionally signifies that even when the nominal worth is similar, the Chinese language’s margin is greater, and European manufacturers could possibly be incentivized to extract the final penny out of their ICEV fashions as a substitute of coming into with much less worthwhile EVs, even when meaning ceding the electrical market to the Chinese language. You already know, make a pleasant revenue now even when the enterprise mannequin goes down the drain in a number of years, and all that.

Finally, low cost power stays a important enter for industrial success, and Europe’s scenario, although a lot improved since 2021, continues to be precarious. The area has considerably freed itself from Russian fuel dependency, however the price has been vital, and the large deployment of renewables (plus nuclear, if maybe France can pull it off as soon as once more) required to forego the expensive LNG has not absolutely materialized but. Europe requires a large quantity of storage, of high-voltage strains to scale back curtailment, and of latest photo voltaic and wind farms if it desires to get power costs to some extent the place it will probably meaningfully compete with China. However even right here, plainly Southern Europe, because of ample solar and large photo voltaic deployment, has been in a position to maintain power costs underneath management, thus offering an industrial base not as affected by excessive prices.

I don’t anticipate 2026 to be a 12 months of sturdy competitors from European manufacturers, as they nonetheless must ramp up and enhance gross sales in native markets to abide by the EU’s emissions requirements. However by 2027, they need to be able to bringing no less than a combat to our shores, lest they find yourself ceding all initiative to the Chinese language. Alternatively, they may depend on native manufacturing (because the Chinese language are doing in Brazil) whereas importing batteries from China or buying native batteries from Chinese language firms, one thing that ought to permit them to beat one among their most vital hurdles.

(I, for one, would love to see Renault’s plant in Colombia churning out inexpensive EVs).

What I do know is that European automakers, traditionally reliant on exports and gross sales in international markets, can’t afford to lose these to the Chinese language, so that they higher begin placing up some competitors. But, it appears, there may be nonetheless hope.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our day by day e-newsletter, and observe us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to counsel a visitor for our CleanTech Speak podcast? Contact us right here.

Join our day by day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if day by day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage