Assist CleanTechnica’s work by way of a Substack subscription or on Stripe.

BEVs on the best way up, PHEVs on the best way down

Plugin car registrations had been up 4% yr over yr (YoY) in Might, ending the month at round 1.7 million items. Curiously, BEVs (+15% YoY) and PHEVs (-15% YoY) had reverse performances, with pure electrics agency in double-digit development whereas plugin hybrids remained within the purple. That is the primary time since 2019 that PHEVs remained within the purple for 5 consecutive months.

This meant that, whereas the plugin YTD numbers are barely optimistic (+2% YoY), that’s solely because of the PHEV blues (-11% YoY). BEVs are on their method again to regular (+9%).

And the completely different dynamics between pure electrics and plugin hybrids are mirrored within the BEV vs. PHEV share of plugin gross sales — in Might, BEVs represented 71% of all plugin gross sales, or about 1.2 million items, among the finest outcomes of the previous few years. That led the YTD breakdown to be 70% vs. 30% in favour of pure electrics, which is touching the ceiling of BEV share of the previous 12 years. Since 2014, BEVs have floated between 70% and 50% of the overall plugin share.

The worldwide BEV takeover vs. China and the USA

The tip of US incentives final October, added to the partial elimination of incentives in China on the finish of 2025, had an anticipated influence, that means that these markets, the third and 1st largest EV markets on the earth, respectively, are dragging down world gross sales.

If we take away China and the USA from the tally, EVs jumped 39% YoY globally in Might, with BEVs surging +47% YoY.

Humorous sufficient, PHEVs are additionally underperforming on this metric, because the 20% PHEV development price in Might, excluding China and the USA, is the bottom for the know-how in over a yr. It’s beginning to appear like PHEVs’ present slowdown is extra structural than anticipated.

Share-wise, Might noticed BEVs finish the month at 19% share, with the tally rising to 26% if we add in PHEVs. This efficiency pushed the 2026 plugin share upward. BEVs elevated their share by one level, to 16%, whereas plugin hybrids remained at 6% share. Due to this fact, the 2026 PEV share is now at 22%.

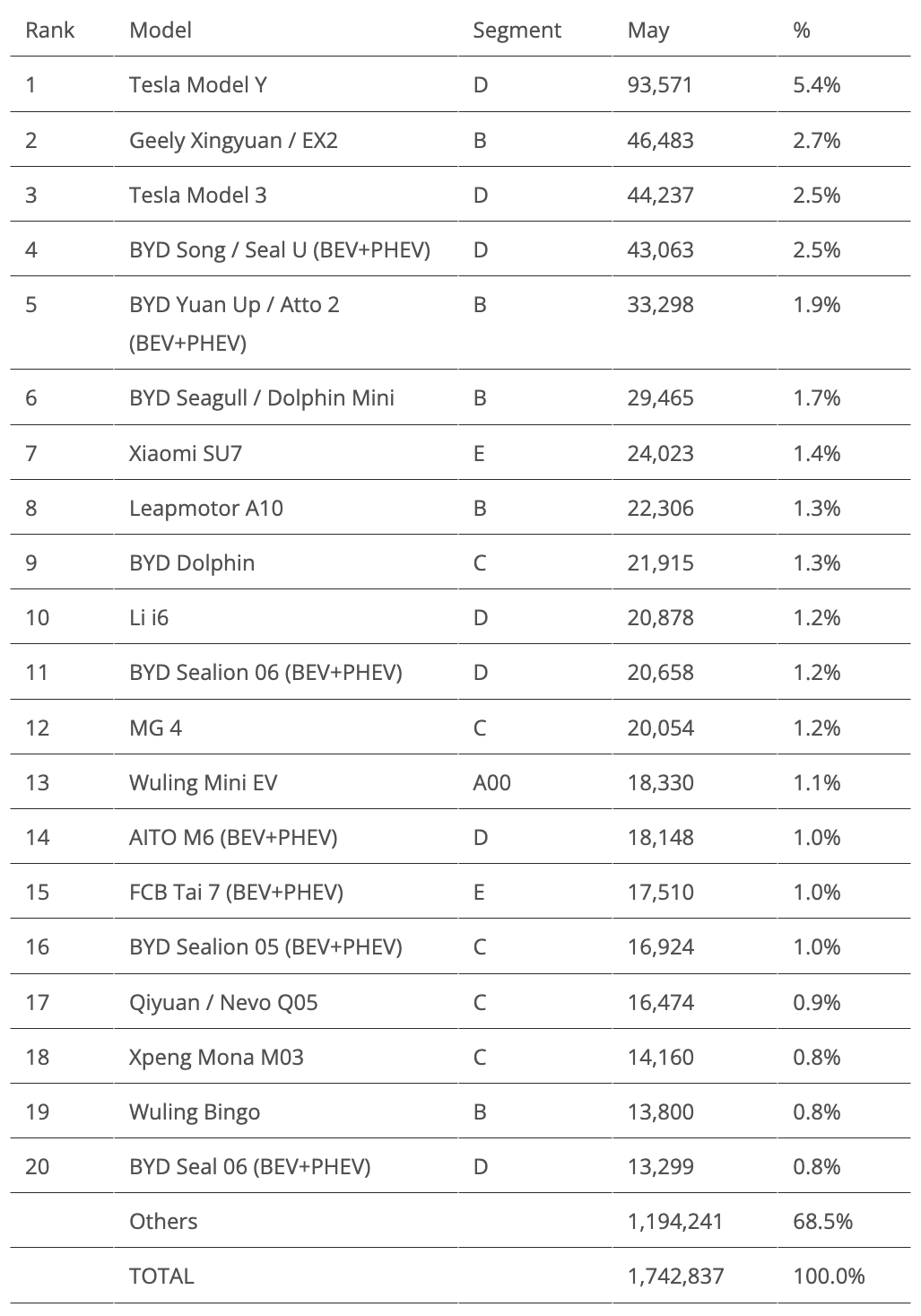

one of the best promoting fashions, one can see that the Chinese language market is recovering quick. As soon as once more, there have been no legacy OEM representatives within the prime 20, and the Tesla Mannequin 3 (44,237 items, up 28% YoY) was as much as third.

Nonetheless, the chief remained the Tesla Mannequin Y (93,571 items, up 16% YoY), which has discovered a renewed youth because of the usual variations and the L three-row physique.

This was sufficient to maintain the Chinese language competitors behind it, just like the Geely Xingyuan (EX2 in export markets), which accomplished the rostrum with some 47,000 registrations, up 20% YoY, in no small half because of export markets. Geely’s small EV is now at cruising velocity, compensating for the lack of demand in its home market with elevated exports.

A shock within the prime half of the desk was the 4th place of the BYD Music. Regardless of being down 18% YoY in Might, its gross sales performances are little doubt rejuvenated by the new-generation Extremely physique, as Might’s 43,000 items represented a brand new yr greatest for the midsize mannequin. Flash charging capabilities promise to recharge the Music’s gross sales and make it a critical candidate for podium positions within the second half of the yr.

One other shock was the fifth place of the BYD Yuan Up/Atto 2. Due to a latest refresh and the launch of a brand new PHEV model, the Up is changing into a star participant within the BYD lineup.

One other spotlight within the first half of the desk is the Leapmotor A10. The recent startup’s new child, a completely electrical small crossover, was eighth. It scored 22,000 registrations in solely its third month available on the market, which is already the greatest place ever for a mannequin from the startup. That might imply that Leapmotor has discovered its star participant, becoming a member of a lineup of constant performers.

Wanting on the second half of the desk, there’s lots to speak about:

- MG positioned its 4 hatchback in twelfth, because of a file 20,054 deliveries. The brand new technology is constructing on the success of its predecessor, and will develop into a critical menace to the management of the BYD Dolphin within the compact class.

- Nonetheless on SAIC, the tiny Wuling Mini EV is slowly recovering, having recorded 18,330 deliveries, a brand new yr greatest. That allowed it finish in thirteenth.

- AITO has a brand new success on its fingers, with the brand new M6 SUV replicating the successful components (giant, comfortable SUVs) within the midsize class. It scored 18,000 deliveries in solely its third month available on the market. Will it’s prime 10 materials quickly?

- One other file scorer was the #17 Qiyuan Q05, with Changan’s mainstream crossover delivering a greatest ever 16,474 items.

- Lastly, we’ve quite a few returns to the desk, with the BYD Sealion 05 in sixteenth because of 17,000 items, its greatest rating in 11 months; the Xpeng Mona M03 18th with 14,000 items, its greatest efficiency since final November; and the new-generation Wuling Bingo bringing the nameplate again to the desk, this time in nineteenth because of 13,800 items, its greatest lead to a yr.

Outdoors the highest 20, there wasn’t a lot to speak about, with the spotlight being the truth that one of the best promoting legacy mannequin belonged to Toyota. The BZ4X registered 11,119 items, forward of the BMW iX1/X1 PHEV twins (10,746 items) and the Hyundai IONIQ 5 (10,478 items). That was its first 5-digit rating since final September, when the US subsidies for EVs had been about to finish. It seems like the worth cuts have introduced the profession of the Korean midsizer again to life within the USA, because the 5,000 items registered there in Might attest.

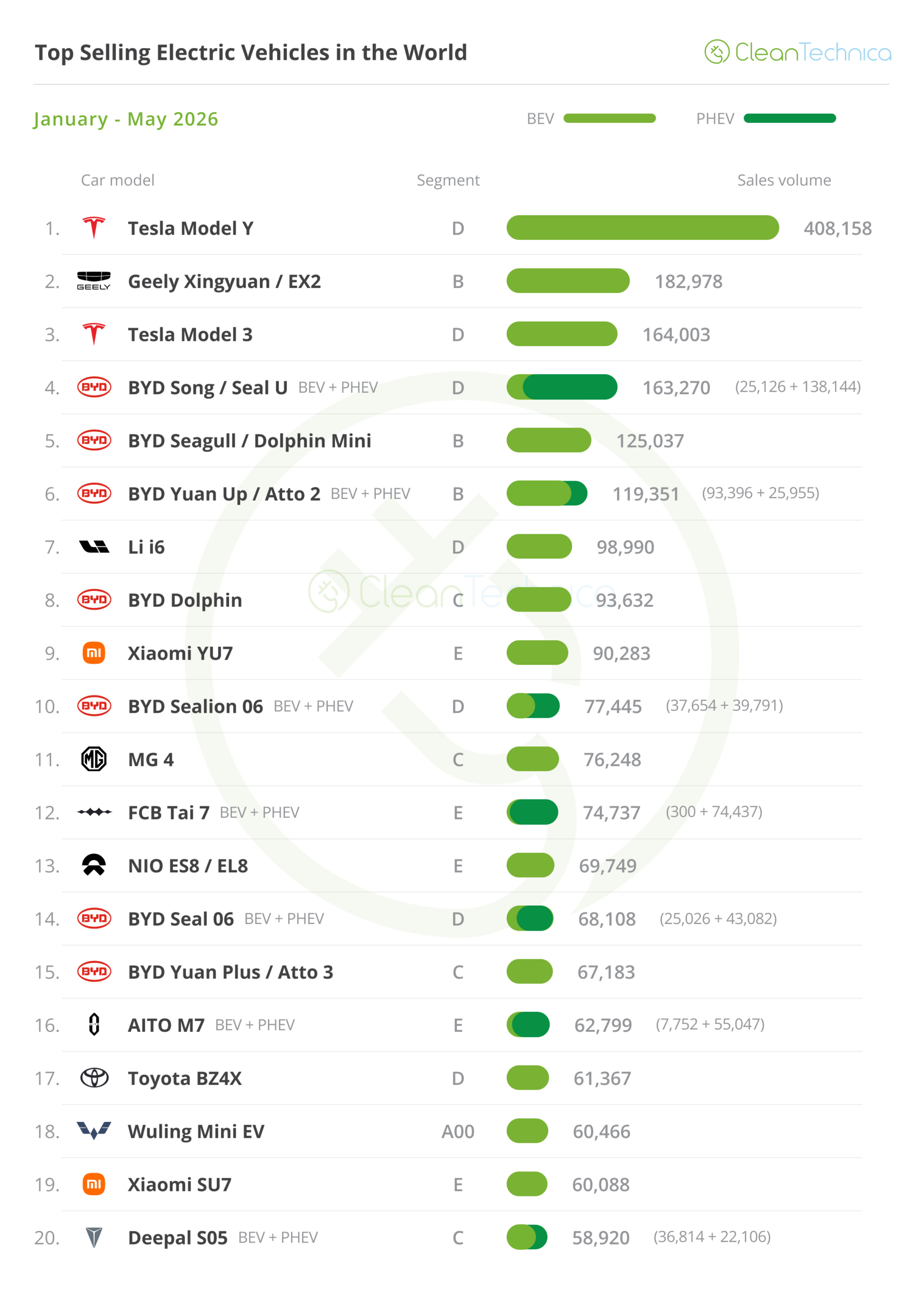

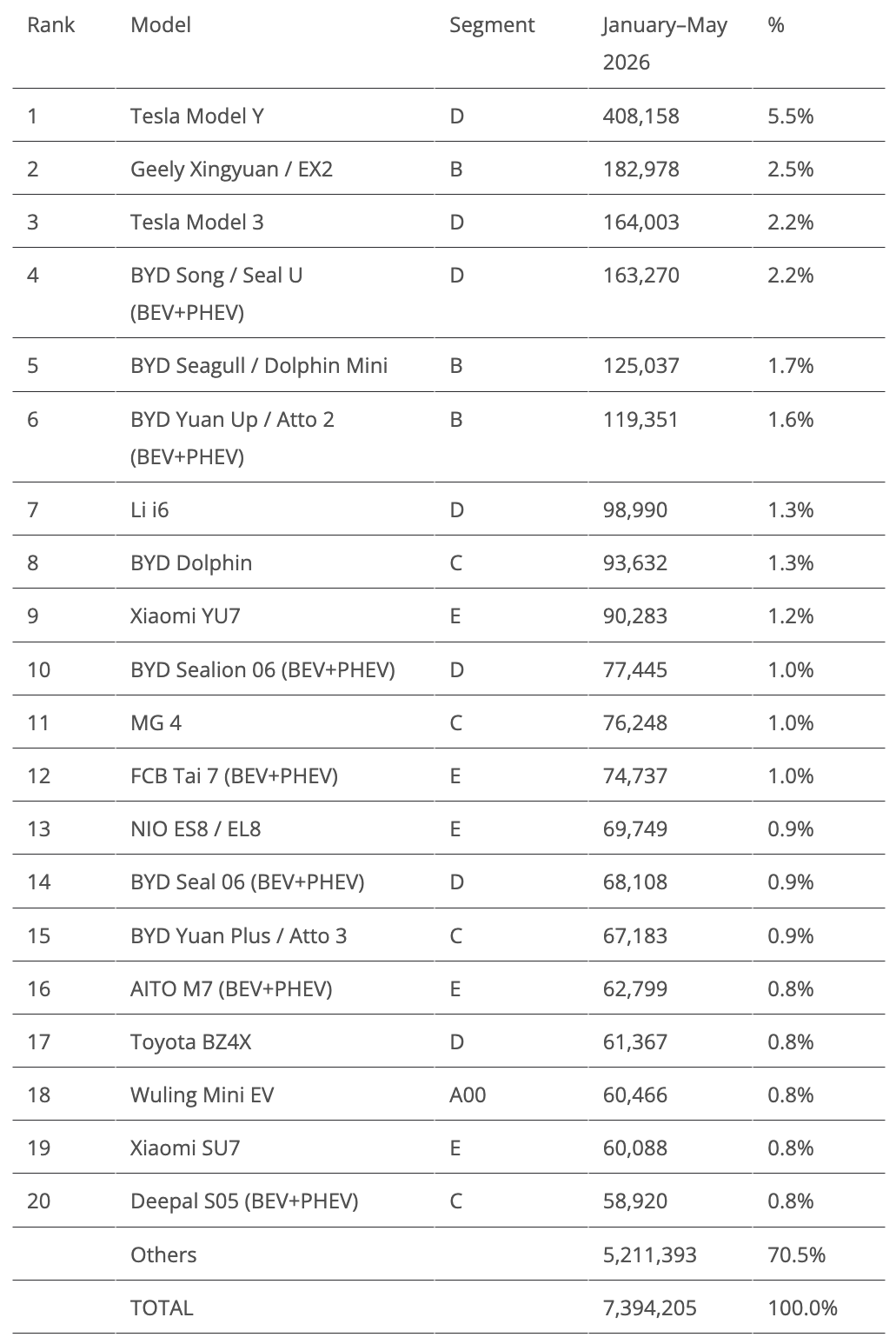

Yr thus far, the chief Tesla Mannequin Y is admittedly in its personal league, promoting twice as many items because the runner-up Geely Xingyuan.

Nonetheless on the rostrum, as anticipated, the Tesla Mannequin 3 gained a bit extra floor over the #4 BYD Music. Count on this distance to widen considerably in June because the Tesla sedan experiences its regular deliveries peak.

However with the Chinese language SUV ramping up a brand new technology in China, and the present one nonetheless promoting in volumes in export markets, will probably be troublesome for the Mannequin 3 to retain a podium place, one thing it has held since 2018.

There have been a pair extra BYDs on the rise, with the Dolphin climbing one place to eighth whereas the BYD Sealion 06 jumped two positions to tenth, thus making it 5 BYDs within the prime 10.

Elsewhere, the MG 4 compact hatchback continues on the rise, leaping two positions to #11, whereas we’ve two returns to the desk — the tiny Wuling Mini EV confirmed up in 18th and the Xiaomi SU7 in nineteenth. This allowed Xiaomi’s two fashions to be current within the prime 20, no small feat for such a brand new automobile model.

Producers: The Rise & Rise of Leapmotor

Nothing actually out of the abnormal occurred on the rostrum, with BYD, Tesla (+20% YoY), and Geely taking excessive three spots.

However behind these three, one thing outstanding has occurred — Leapmotor scored one other file consequence, with greater than 81,000 registrations, ending Might in 4th. It ended the month fewer than 9,000 items behind Geely. With a slew of recent metallic coming (A10 small crossover, A05 small hatchback, D19 giant SUV, D99 giant MPV…), count on the startup’s gross sales to proceed rising considerably. So, Geely should be careful.

One other spotlight was Zeekr, which ended the month in tenth with a file 34,377 registrations, all because of the success of its full measurement 9X and 8X giant SUVs, which collectively had 15,000 registrations. There’s additionally the success of the 7X midsizer — because of export markets, it has seen its gross sales enhance to six,700 items.

Concerning the remaining positions on the desk, one other shock was the file rating of Changan’s Qiyuan, which delivered a file 29,264 items. That put it within the #20 spot. Its success was particularly because of the success of its compact crossover, the Q05.

Lastly, a reference is due for Hyundai, in seventeenth, with 31,000 registrations. It was its greatest rating since final September, with the IONIQ 5 being the model’s spotlight.

Leapmotor surpasses Volkswagen

As for the year-to-date desk, there was no main information on the rostrum, however proper under it, issues are altering.

Leapmotor is now … 4th. Bye bye, BMW. So lengthy, Volkswagen. A Chinese language startup has simply surpassed you.

And whereas that is no main drama for BMW — in any case, being this excessive up within the rating is an anomaly, contemplating that the Bavarian OEM is barely thirteenth within the general automotive rating. The identical can’t be stated about Volkswagen. No marvel they’re now taking drastic measures….

One other Chinese language model going up is Wuling. It climbed to sixth because of the new-generation Bingo and the restoration of the Mini EV. I wouldn’t be shocked to see it additionally quickly surpass Volkswagen….

Wanting on the second half of the desk, Xiaomi was up one spot, to eleventh, having surpassed Mercedes. So, a two-year-old model, which is a part of a smartphone portfolio, has outsold the oldest carmaker on the earth.

Last mentions go to Hyundai, which was as much as sixteenth because of robust gross sales of the IONIQ 5 within the USA, and #18 AITO, which is now using the wave of its new M6 mannequin.

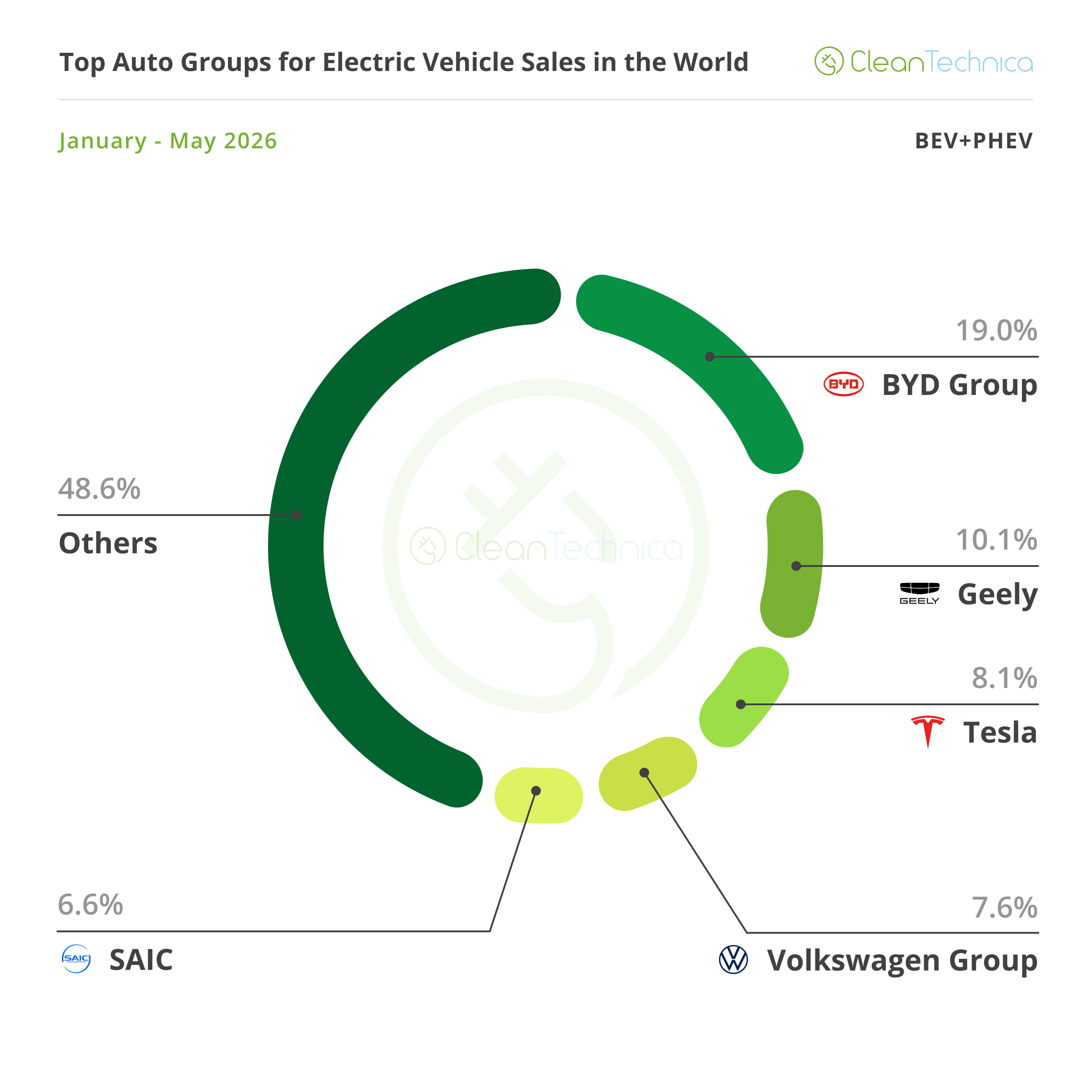

OEMs, BYD (19%) is steady within the lead, whereas runner-up Geely (10.1%) has benefitted from the nice outcomes of Zeekr and its namesake model.

#3 Tesla (8.1%, up from 8% in April) stayed forward of Volkswagen Group (7.6%), so it appears that evidently the OEM is assured a podium place this yr.

#5 SAIC remained in fifth, with 6.6% share, whereas Hyundai–Kia (4.2%) is the brand new sixth positioned OEM, having surpassed Chery (4.1%).

#8 Changan (3.9%) is now seeing a rising Leapmotor (ninth, 3.6% share) getting shut, so we’d see a place change right here, and Toyota can also be beginning to seem on the radar, with the Japanese OEM now in eleventh with 2.8% share.

Wanting simply at BEVs, there have been about 5.2 million registrations to this point this yr, or 70% of whole plugin gross sales. Will they finish the yr above 75%? If that’s the case, that might be their greatest consequence since 2012....

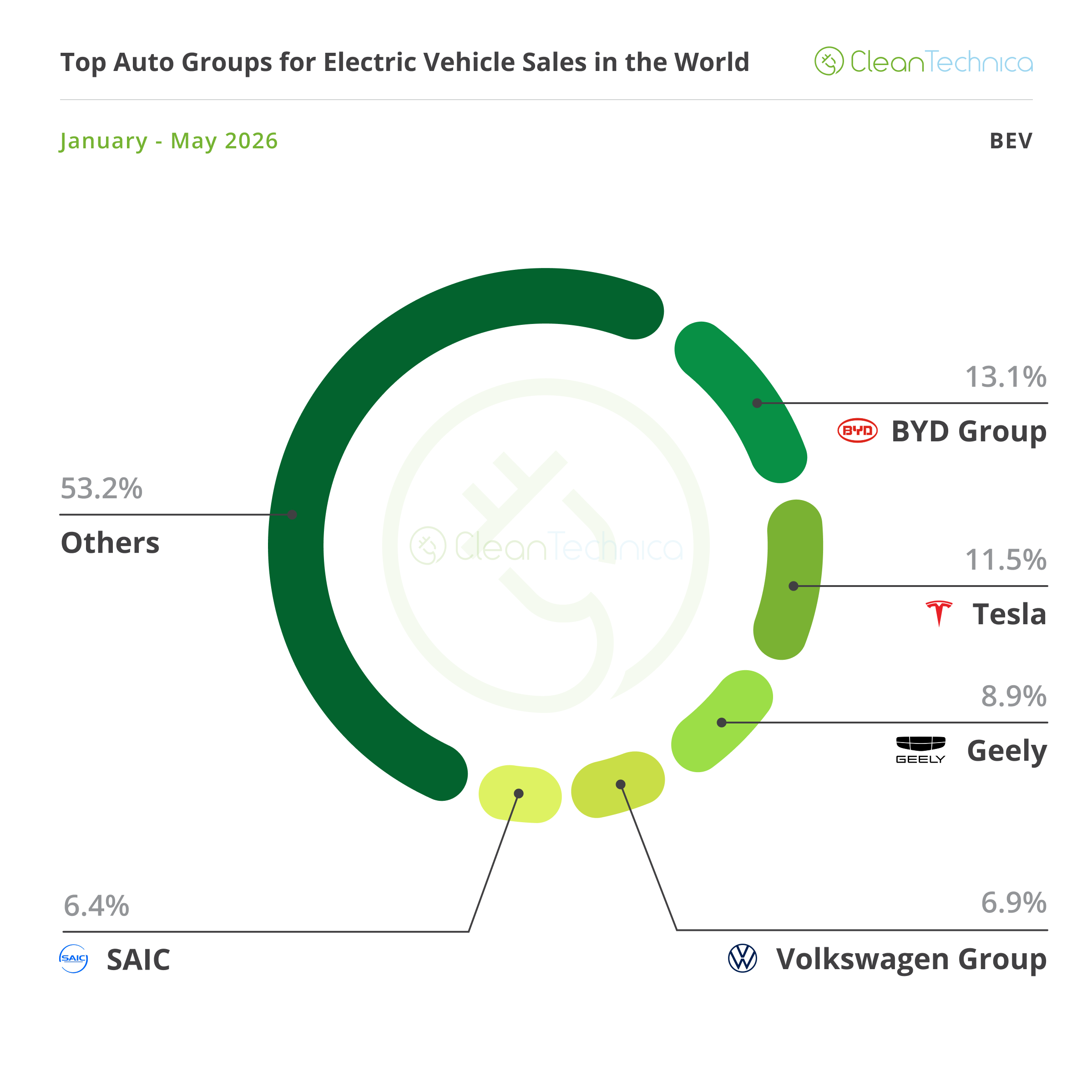

On the prime, Tesla (11.5%) is steady within the runner-up spot, whereas chief BYD (13.1%) appears to have gained sufficient benefit to maintain Tesla at bay (the Texan may have its regular peak month in June).

In third place, we’ve Geely (8.9%), conserving #4 Volkswagen Group at bay (6.9%, down 0.1% share). In the meantime, #5 SAIC (6.4%, up from 6.3% in April) is beginning to attain the again of the German OEM.

Outdoors the highest 5, #6 Hyundai–Kia (4.8% share) is the one OEM near the highest 5 makers.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our every day e-newsletter, and comply with us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage