Grey Hydrogen, Excessive Prices, and the Actual Emissions of SunLine’s Gasoline Cell Fleet

Help CleanTechnica’s work by a Substack subscription or on Stripe.

SunLine Transit Company, which offers transportation for the massive western California county that features Palm Springs and Coachella, has spent 1 / 4 century doing greater than nearly any transit company in North America to attempt to make hydrogen buses work. It began hydrogen manufacturing and meting out round 2000, has cycled by electrolyzers, reformers, a big PEM electrolyzer station, and now a liquid hydrogen station, and has operated or examined a protracted listing of hydrogen automobile sorts alongside the way in which. If hydrogen transit was going to mature right into a sturdy working mannequin wherever, a small desert company with lengthy expertise, supportive regulators, and a willingness to maintain rebuilding the system regarded like a very good candidate.

What SunLine has really constructed is one thing extra revealing and extra sobering. It’s not a single mature hydrogen ecosystem that has run steadily for many years. It’s a chain of successive initiatives, upgrades, repairs, replacements, and new funding rounds, all in service of protecting a specialised fueling and automobile system alive.

The early years matter as a result of they present the sample from the beginning. SunLine’s milestones file an 84 kg/day electrolyzer in 2000, then a 216 kg/day HyRadix auto-thermal reformer in 2004, then a industrial 228 kg/day HyRadix Adéo reformer in 2006. Alongside that fueling evolution got here a rolling mixture of bus applied sciences and suppliers. SunLine’s timeline contains the Ballard ZEbus demonstration, HCNG buses, HHICE buses, a Van Hool gas cell bus, the American Gasoline Cell Bus program, and later New Flyer gas cell buses. That churn just isn’t incidental. It means SunLine was not working one steady, mature expertise stack. It was collaborating in an prolonged demonstration ecosystem through which each the buses and the fueling programs stored altering.

The refueling historical past is finest understood as 4 generations. The primary was the early pilot electrolyzer and small demonstration fueling setup. The second was the reformer period, beginning with the ATR prototype after which the industrial reformer, plus upgrades to meting out, compression, and storage. The third was the massive bounce to a 900 kg/day PEM electrolyzer station accomplished in late 2019. The fourth was the addition of a liquid hydrogen station commissioned in 2024 so as to add resiliency and fueling velocity to the positioning. That sequence is essential as a result of it reveals that SunLine didn’t construct a station within the early 2000s after which merely function it. It rebuilt the hydrogen system time and again as every technology proved inadequate, unreliable, or too small for the subsequent stage of ambition.

The capital historical past makes the identical level extra sharply. Utilizing printed challenge figures the place accessible and outside-view estimates the place SunLine didn’t disclose a clear all-in quantity, the refueling system provides as much as about $27M in 2026 {dollars} throughout the foremost milestones now seen within the public file. That features the early electrolyzer, the prototype ATR reformer, the industrial SMR reformer, the 2009 compression and storage growth, the 2011 compressor restore episode, the 2016 PSA mattress and valve alternative, the 2019 PEM electrolyzer construct, and the 2024 liquid hydrogen station. Nevertheless one slices the small print, the image is identical. Roughly $27M of refueling capital has been spent or dedicated in 2026 {dollars} to assist a hydrogen fleet that at this time is on the order of 31 to 32 buses.

That spending didn’t purchase low gas price. SunLine’s hydrogen economics have been excessive and unstable for years, and the general public file reveals the company knew it. NREL reported hydrogen price at SunLine averaging $17.21/kg within the 2007 to 2008 interval and explicitly stated the excessive price was because of low station use. Later NREL reporting confirmed common hydrogen price at $26.19/kg throughout the 2010 to 2011 interval after compressor issues. One other SunLine and NREL analysis confirmed common hydrogen price at $12.15/kg, however with month-to-month values starting from $6.50/kg to $158/kg as utilization and upkeep shifted. The later PEM-electrolyzer period improved a number of the economics, with NREL reporting $13.79/kg in a single analysis interval, however that’s nonetheless costly gas for transit service. The sample just isn’t that hydrogen obtained steadily low-cost over time. The sample is that hydrogen remained expensive, and the associated fee per kilogram moved round with utilization, repairs, and station configuration. For the sake of this comparability, I normalized all prices per kg to 2026 greenback values and ensured that every one had the price of hydrogen and the amortized price of infrastructure, as reporting different through the years.

SunLine additionally needed to stay with the restore and reliability aspect of that economics. NREL documented a significant compressor failure in 2011 that drove price upward. In 2016, SunLine needed to change strain swing adsorption mattress materials and a valve, and the station was down for about eight weeks whereas ready for elements. Throughout that outage, the company introduced in delivered hydrogen and restricted bus service as a result of delivered hydrogen price greater than on-site manufacturing. The transition to the 900 kg/day PEM electrolyzer didn’t finish these points. CARB’s ultimate challenge report on that station described a tough commissioning interval with 35% downtime in December 2019 alone, plus low CO2 compressor ranges within the pre-cooling system, an undersized cooling system, compressor packing failure, and a heater failure within the drying system. This isn’t proof of incompetence. It’s proof that hydrogen refueling stays a specialised and maintenance-heavy system even in one of the vital skilled businesses on the continent.

That’s one purpose the liquid hydrogen station issues. The general public case for it was resiliency and capability. The California Vitality Fee awarded about $5M in 2021 for a stand-alone liquid hydrogen station, and Nikkiso later stated the station might gas SunLine’s present 32-bus fleet and fill a bus in underneath 10 minutes. AQMD offered one other million and indicated the station might gas as much as 50 gas cell buses. Operationally, that is sensible. If the electrolyzer advanced has been troublesome and the fleet is bigger, a truck-delivered LH2 backup and growth path is enticing. However it is usually a quiet admission that SunLine’s lengthy pursuit of on-site hydrogen didn’t produce a easy, strong fueling mannequin that might stand alone. The reply to troublesome hydrogen infrastructure turned out to be extra hydrogen infrastructure.

To be clear, SunLine wasn’t spending that a lot on the hydrogen itself by a lot of this. The DOE and California paid for many of the hydrogen refueling infrastructure, so the amortization of capital burden wasn’t on SunLine’s e-book. They possible assisted with the foremost refurbishment prices as properly. If SunLine had been paying for its personal hydrogen, it might have stopped experimenting with hydrogen way back.

The emissions implications of that shift aren’t flattering. SunLine’s earlier reformer pathway was unabated SMR hydrogen, which in all fairness estimated at round 9 to 12 kg CO2e/kg H2. The present liquid hydrogen seems to be truck-delivered LH2, and I didn’t discover public proof that it’s licensed renewable. The most effective analytical assumption is that it’s typical fossil hydrogen that has additionally paid the vitality and transport penalty of liquefaction and supply. Possible they assumed that it might develop into inexperienced hydrogen when ARCHES constructed large electrolyzers. That pushes possible emissions to roughly 14 to 18 kg CO2e/kg H2. Utilizing SunLine-specific NREL bus effectivity of seven.05 miles/kg H2 and a typical 45,000 miles per yr obligation cycle, every bus consumes about 6,383 kg H2 per yr. A 31-bus fleet due to this fact makes use of about 197,872 kg H2 per yr. At 15 to 16 kg CO2e/kg H2, that fleet emits roughly 2,968 to three,166 tons CO2e per yr.

The diesel comparability is uncomfortable for a expertise usually described as clear. Utilizing a consultant diesel transit bus determine of 4.14 mpg and diesel combustion emissions of about 10.21 kg CO2 per gallon, an equal diesel fleet working the identical annual distance would emit about 3,440 tons CO2 per yr. Meaning SunLine’s hydrogen fleet, if fueled primarily with typical delivered LH2, is just round 8% to 14% decrease in annual emissions than diesel underneath these assumptions. A zero-tailpipe fleet can nonetheless be a excessive upstream emissions fleet. SunLine’s hydrogen buses aren’t near-zero carbon if they’re leaning on grey liquid hydrogen. They’re simply considerably higher than diesel whereas being way more capital-intensive and operationally specialised.

The distinction with battery-electric is revealing, and never in hydrogen’s favor. California’s personal bus market reveals that battery-electric has develop into the dominant zero-emission pathway. As of July 2025, CALSTART counted 1,933 battery-electric transit buses in California versus 690 gas cell buses. My latest evaluation discovered 2023 noticed peak orders for extra gas cell buses, with vital drops in 2024 and solely 15 in 2025, whereas battery electrical buses proceed to be bought. SunLine has round 4 as properly, and said plans to develop that to 18. Tailpipe emissions for the battery electrical buses charging at California’s grid depth, are about 20% that of diesel’s, and they are going to be declining every year as California continues to decarbonize its grid. Keep in mind, the purpose of low-emissions buses is low emissions. Battery electrical delivers that. Hydrogen isn’t delivering that.

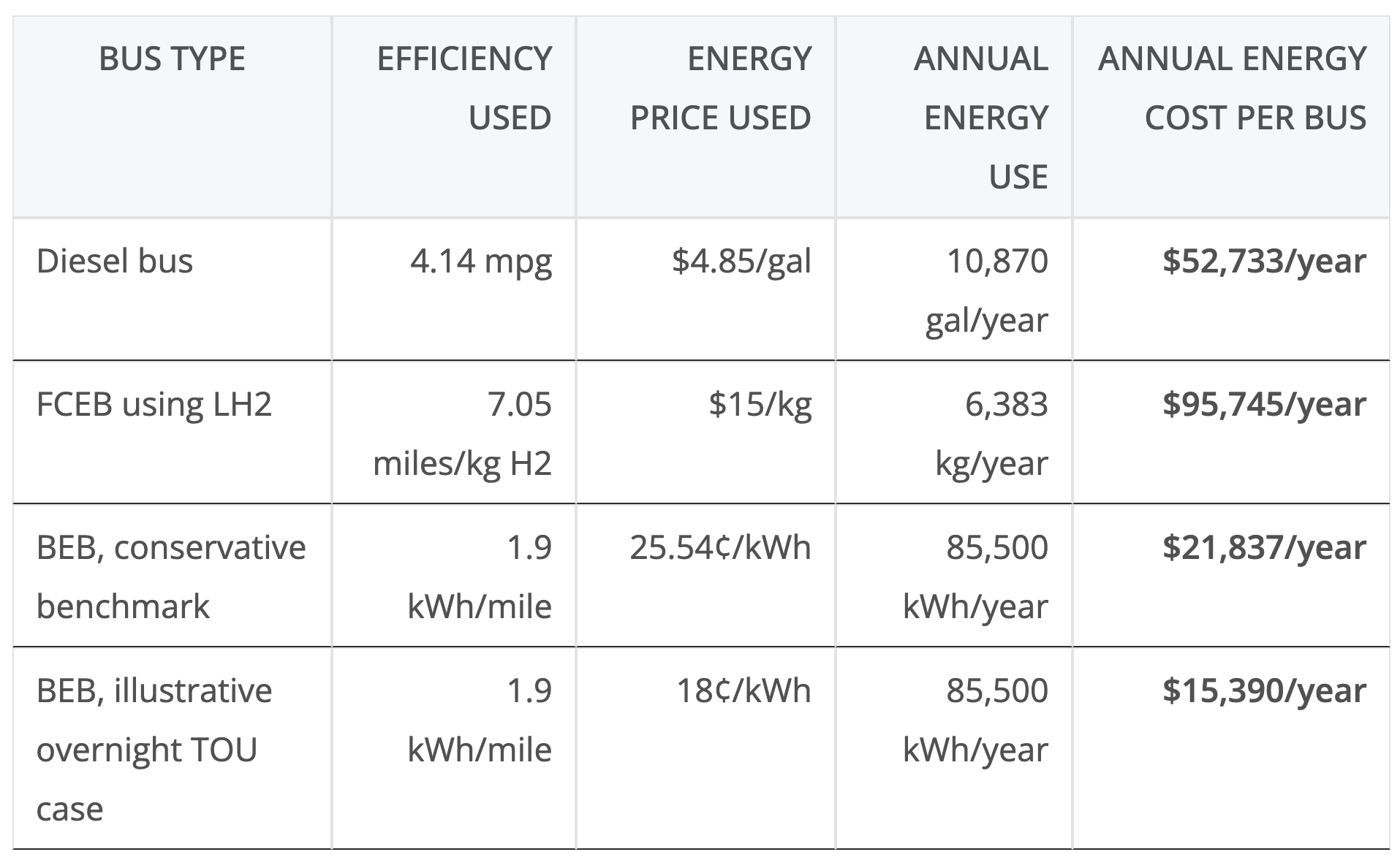

Utilizing the identical 45,000 miles per bus-year as the sooner emissions comparability, the energy-cost hole is extreme. A consultant diesel bus at 4.14 mpg and California’s 2025 common diesel worth of about $4.85/gal is available in at roughly $52,700 per yr for gas. A fuel-cell bus at 7.05 miles/kg working on SunLine-style LH2 at about $15/kg is available in at roughly $95,700 per yr. A battery-electric bus at 1.9 kWh/mile charging at California’s common industrial electrical energy fee of 25.54¢/kWh would price about $21,800 per yr, and at a extra believable in a single day charging fee of 18¢/kWh would price about $15,400 per yr. In different phrases, every hydrogen bus is burning about $73,900 to $80,400 extra per yr in vitality than a BEB protecting the identical distance. Throughout SunLine’s 31 fuel-cell buses, that means roughly $2.29M to $2.49M extra in annual vitality price than if those self same 31 buses had been battery-electric, earlier than even contemplating the additional upkeep burden and refueling infrastructure prices that include hydrogen.

That brings the dialogue to ARCHES and the long run. Hydrogen transit programs want cash for buses, for fueling, for storage, for compressors, for chillers, for repairs, and finally for replacements of specialised tools that no diesel or battery-electric fleet supervisor has to consider in the identical manner. Foothill Transit’s 2025 board supplies had been the clearest instance of what occurs when a significant funding layer disappears. DOE’s ARCHES-related assist was terminated, eradicating $300,000 per bus, 1,000,000 {dollars} to repair their three yr outdated refueling station, and one other $1.4 million to broaden with one other refueling station, whereas California’s HVIP program remained oversubscribed and unsure. Employees responded by recommending a shift away from hydrogen as a result of doing so would save about $27.6M upfront and about $1.8M per yr in gas price. SunLine is a unique company with an extended hydrogen historical past, however the structural dependency is comparable. With out ARCHES-scale capital assist or one thing near it, the subsequent spherical of station overhauls, part replacements, and bus procurements turns into tougher to finance.

That is the danger now hanging over SunLine’s 31 hydrogen buses. The company has already proven that it might function them. That isn’t the identical as displaying it might assist them economically over the subsequent decade with out one other main wave of outdoor funding. If the liquid hydrogen station turns into the popular fueling pathway as a result of it’s less complicated to function than the electrolyzer advanced, SunLine turns into extra depending on truck-delivered grey hydrogen with greater embedded emissions. If the PEM station and related tools proceed to want fixes and upgrades, SunLine will maintain needing capital. If alternative gas cell buses stay costly and the remainder of California retains transferring towards BEBs, hydrogen bus procurement turns into tougher to justify on pure economics. The possible consequence just isn’t an instantaneous collapse. It’s a grinding monetary drawback through which the company is left supporting a capital-heavy, maintenance-heavy, emissions-compromised hydrogen system with fewer massive grant applications keen to hold the load.

The most recent and sure most sturdy piece of SunLine’s hydrogen system is the 2024 liquid hydrogen station, which implies it is usually the asset more than likely to find out when the company faces its subsequent actual strategic determination. There is no such thing as a clear business rule saying an LH2 transit station lasts a hard and fast variety of years earlier than main recapitalization, however the exterior view just isn’t encouraging. NREL’s hydrogen-station reliability work reveals that dispenser, compressor, and chiller programs dominate upkeep occasions, with failure frequencies far greater than typical fueling programs.

SunLine’s personal historical past factors the identical manner. Its hydrogen infrastructure has wanted a significant rebuild, alternative, or restore cycle roughly each 4 to 5 years, transferring from early electrolyzers to reformers, then by main compressor and PSA repairs, then into the PEM electrolyzer rebuild and now the liquid hydrogen station. For the LH2 station itself, the civil works and tank shell might final a decade or extra, however the cryogenic pump, vaporizer prepare, controls, dispenser {hardware}, and related stability of plant are more likely to drive a significant refurbishment sooner. On that foundation, the primary severe recapitalization window is probably going round 2029 to 2031, with 2030 the central case.

That timing issues as a result of the 2024 LH2 station is clearly the operational spine for SunLine’s roughly 31 hydrogen buses. If it reaches a significant refurbishment level round 2030, the company is unlikely to be a minor expense. An affordable outside-view estimate is {that a} midlife refresh would price about 20% to 35% of authentic capex, which on the roughly $14.55M 2026-dollar station estimate implies one thing like $2.9M to $5.1M. A extra intensive overhaul might rise into the $5.8M to $8.7M vary.

If ARCHES-scale funding doesn’t return, an final result I take into account possible now that the hydrogen hype bubble has light globally, that’s the level at which SunLine’s hydrogen future turns into a lot tougher to defend economically. The company could be deciding whether or not to place a number of million extra into protecting a gray-hydrogen fueling system alive, with all the upkeep and provide danger that means, or begin directing that cash towards a battery-electric transition with less complicated infrastructure, decrease operational prices and a wider market behind it. My expectation is that SunLine will park its fleet prematurely and completely in 2030 or 2031, as Aberdeen simply did. After all, a completely rational transit company would have regarded on the clear outcomes of 20 years of very excessive prices and excessive precise emissions and pivoted to battery electrical buses by 2019.

SunLine deserved respect for persistence and technical ambition within the 2000s. By the 2010s it was questionable what they had been proving, however no less than the variety of buses remained a small fraction of their 140 bus fleet. It has finished greater than nearly any transit company to provide hydrogen buses a good trial over a few years and plenty of expertise cycles. Growth since 2019 was a strategic mistake, as that lengthy historical past factors to a conclusion that’s troublesome to keep away from. Hydrogen transit at SunLine has not matured right into a low-cost, low-risk, low-carbon working mannequin. It has remained a sequence of costly infrastructure generations, specialised automobile procurements, restore episodes, and policy-supported pivots in gas provide. With ARCHES gone and no signal that hydrogen economics have crossed into self-sustaining territory, SunLine appears much less like a glimpse of transit’s future and extra like a well-funded case research in how onerous it’s to maintain hydrogen buses working in any respect.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summaries, join our each day publication, and observe us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our each day publication for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if each day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage