Help CleanTechnica’s work by means of a Substack subscription or on Stripe.

After the standard December EV report gross sales peak in China, which coincided with an end-of-incentive gross sales rush (NEVs are not exempt from buy tax this yr), the yr began with an anticipated gross sales stoop, down by 20%, which appears like so much, however contemplating that the general market was additionally down 14% YoY, to 1.5 million models, it doesn’t sound all that unhealthy.

BEVs had been down by 17% YoY in January, to 348,000 models, whereas the PHEV drop was even harsher (-24%), at 248,000 models. Of those, 76,000 had been EREVs, which is likely one of the few brilliant spots of January. The extended-range electrical automobile market was truly up 1% YoY, because of the recognition of this type of powertrain in giant SUVs, which was the class much less affected by the tip of incentives.

This allowed plugin automobile (PEV) share to begin the yr at a excessive 39% (23% BEV), roughly aligned with January ’25, which is sweet information contemplating the lack of incentives. Though this rating is nicely under the ultimate 2025 results of 54% PEV share (33% BEV), anticipate that mark to be achieved someday in the summertime, and the yr to finish round 60% share. A few months within the final quarter of the yr ought to even finish above 65% share.

Think about that — the most important automotive market on this planet with a 66% plugin share. These sorts of market shares could be thought of a pipe dream once I began reporting EV gross sales again in 2012….

Within the total rating, as anticipated, the start of the yr has ICE fashions populating the highest 10 — seven fashions within the high 10, in actual fact. This yr, there’s a sense that the market is shifting. For starters, now we have a model new mannequin on high, with the Xiaomi YU7 sporty crossover successful the general trophy for the primary time ever. Behind it, there was a small revolution underway. The remaining podium positions went to 2 Geelys (Geelies?), with the Geely Boyue L ICE successful silver and the Geely Xingyuan hatchback successful bronze.

Humorous sufficient, essentially the most represented manufacturers within the high 10 had been Geely and … Volkswagen(!), with the German make inserting three ICE fashions, giving a sure retro really feel to the general high 10. The AITO M7 was the third plugin mannequin, in fifth.

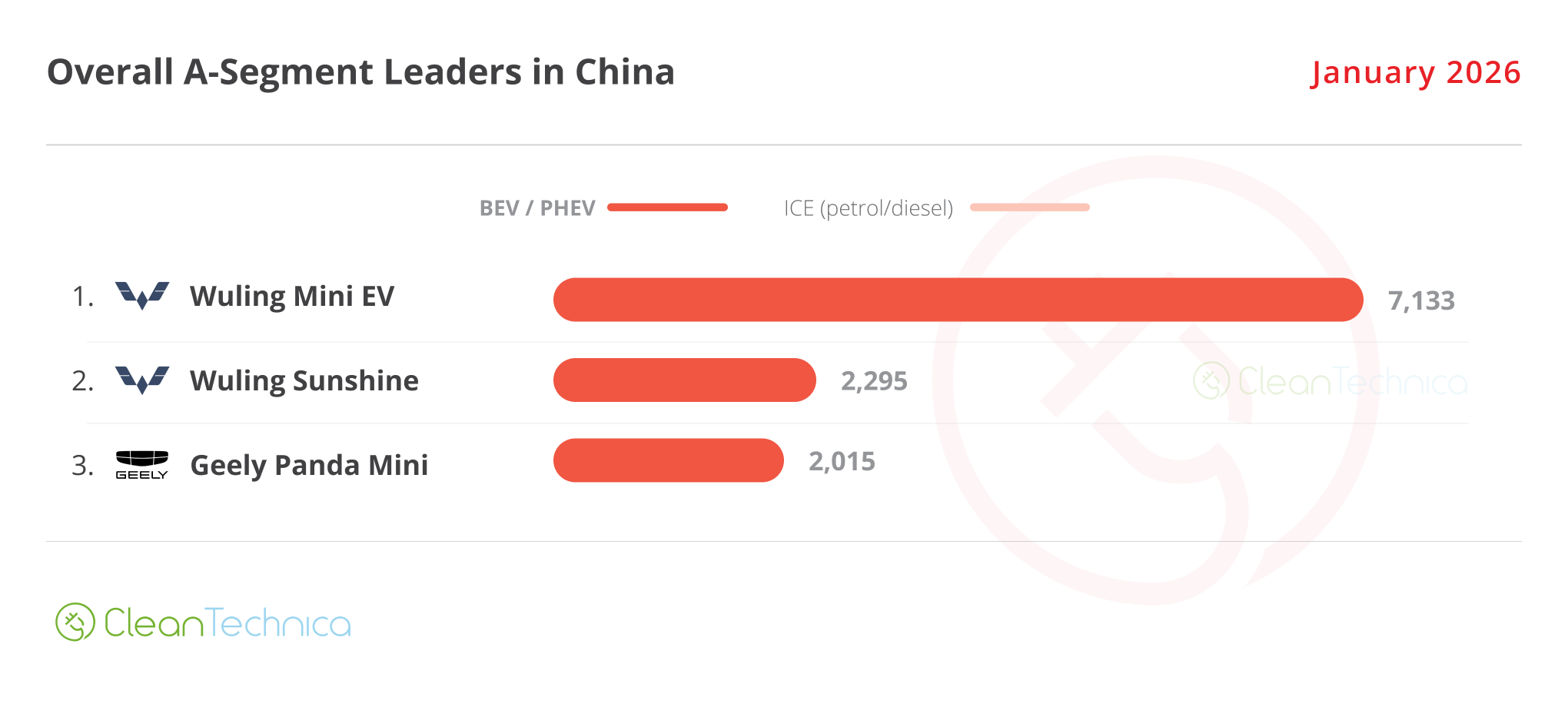

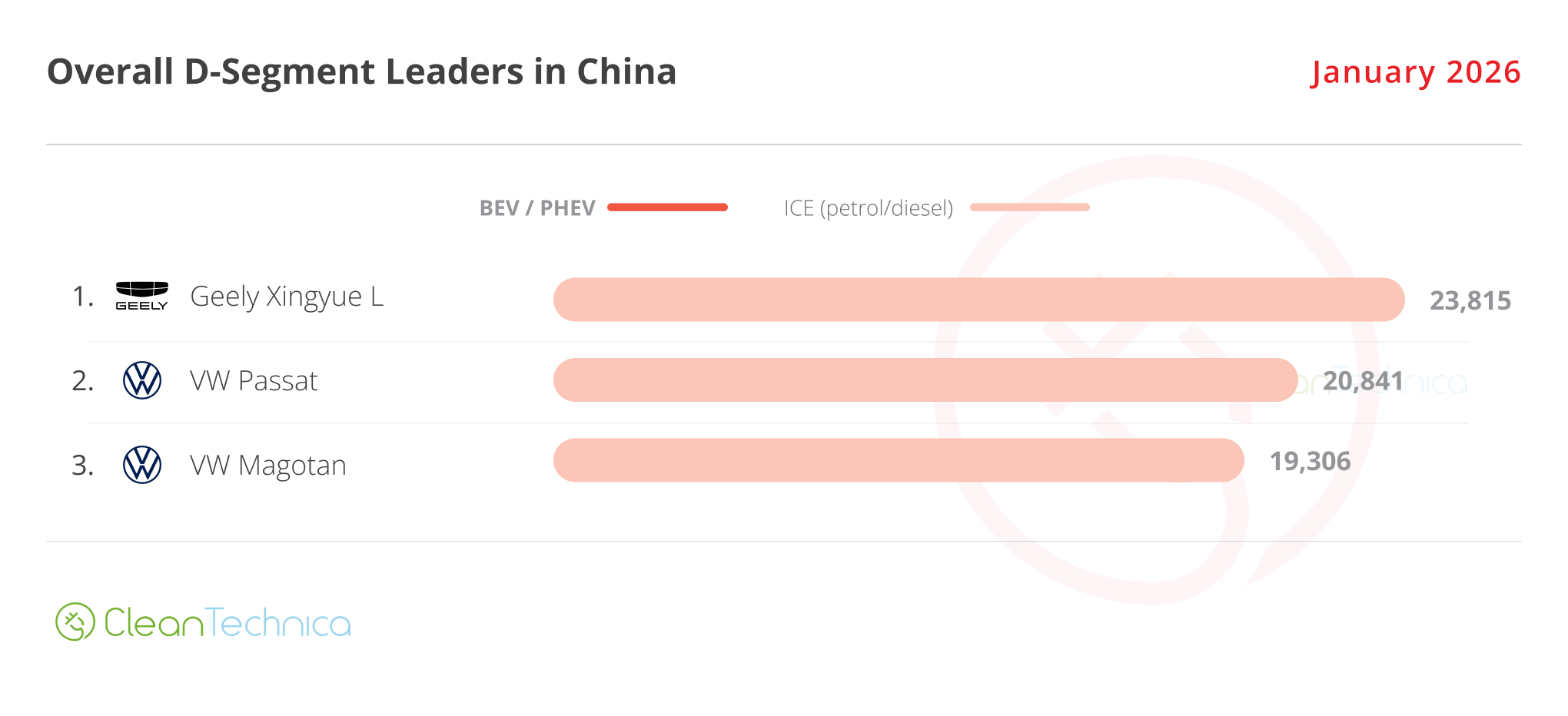

Taking a look at the most effective sellers in a number of dimension classes, all however the C (compact) and D (midsize) segments have plugins main every class. In truth, in these two classes, all high three positions had been stuffed by ICE fashions.

The largest surprises had been the Geely victories within the C and D segments — from the ICE fashions Boyue L and Xingyue L, respectively.

They’ve crushed the lacking in motion BYD competitors and Tesla Mannequin Y, which haven’t even joined the rostrum in these dimension classes! It was an excellent month for Geely, which positioned 5 representatives on the class podiums, all whereas BYD had … zero. Nada.

It is a entire letter of intention from Geely. With Geely’s sprawling lineup, albeit nonetheless partly counting on ICE (inside combustion engines), the actual fact is that if BYD thought it had the Chinese language market locked in for the following few years, it might need been incorrect and Geely might be the one to spoil BYD’s plans…. Possibly already this yr.

Focusing solely on plugins, and illustrating the altering traits of the Chinese language EV market, solely the Geely Xingyuan has repeated its high 5 presence 12 months later. And all high 5 positions went to 5 totally different OEMs. Now that’s what I name (welcome) range!

Right here’s a better take a look at January’s high 5 finest promoting fashions:

#1 — Xiaomi YU7

2025’s Automobile of the 12 months, Xiaomi’s YU7 continues to impress, registering a near-record 37,869 deliveries in January and amassing its first month-to-month finest vendor award. The YU7 acquired lots of of hundreds of locked-in orders inside hours. So, a partial lack of incentives couldn’t gradual issues down for the sporty crossover, as Xiaomi nonetheless has a large ready record for its new star participant. The YU7 will certainly be a mannequin that can accumulate loads of podium presences (and wins?) within the coming months.

#2 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull cash — at the least, that’s how Geely’s inside memo might need described the Geome Xingyuan when creating its newest hatchback. And with an attention-grabbing identify, as Xingyuan interprets as “wishing upon a star,” is Geely hoping on a star to take BYD’s management place? Effectively, that’s what the Xingyuan did within the B-class class. It obliterated BYD’s fashions in addition to the remainder of the competitors, with none margin of doubt. What does this hatchback have that makes it so particular? Moreover all of the help that comes from a number one OEM like Geely, it has a rounded, smart design, someplace between a Wuling Bingo and a Sensible #3. Beginning with an 80,000 CNY (+/-$11,000) value, the customer will get a 30 kWh LFP battery from CATL, which is nothing to jot down house about till you realise that its value locations it nearer to the BYD Seagull (70,000 CNY for the 30 kWh model) than the BYD Dolphin (100,000 CNY). In January, the Geely mannequin hit 29,007 registrations.

#3 — AITO M7

The second era AITO M7 is one other instance of the progress that Chinese language EVs are making. After beginning out its profession in 2022, with an okay(ish) design and already respectable specs (EREV powertrain, 40 kWh battery), regardless of being based mostly on an ICE platform, solely three years later, in 2025, a model new era has launched — with a sleeker design, fully new platform, improved specs (53 kWh battery for the EREV model, 100 kWh for the brand new BEV model), all for round $35,000. Which isn’t a foul value for a full dimension, three row SUV….

#4 — NIO ES8

Because of the brand new era, the third ever because it was launched in 2018, NIO’s large SUV scored 17,645 registrations in January, offering the startup firm its first high 5 end and far wanted quantity in its quest to achieve profitability. Not precisely low cost — it begins at round $57,000 — the reality is that NIO has thrown every little thing it has into the brand new ES8. The corporate is seeking to redefine luxurious with its new, enormous SUV, now at 5.3 meters. Will this stage of gross sales be sustainable sooner or later? A yr in the past, I might say it was unlikely, however with large SUVs being the newest vogue development in China, and BEVs outrunning PHEVs not too long ago, it might be the case that the ES8 is likely to be the proper mannequin on the proper time.

#5 — Fang Cheng Bao Tai 7

BYD’s premium arm Fang Cheng Bao has a hit on its fingers. This large Land Rover SUV, the Tai (Ti?) 7, scored 17,116 registrations final month. This Chinese language Defender has an EREV powertrain with both 27 or 36 kWh batteries, permitting round 100 km (60 miles) of vary — which could not sound a lot in comparison with the 52 kWh battery of the Lynk & Co 900, one other Land Rover-inspired EREV SUV, 0r the 70 kWh of the Zeekr 9X, the Rolls Royce–impressed flagship EREV SUV from the Geely steady, however then once more, the Tai 7 ($25,000) is nearly half the value of the Lynk & Co mannequin and nearly one third of the value of the Zeekr…. Because of a profitable boxy design, aggressive specs, and a pleasant inside, for its value vary, that is a type of fashions that simply begs to be despatched abroad — going after not solely the posh SUVs of premium manufacturers, but in addition the fuel guzzling Land Cruisers and Patrols of this world.

Beneath the highest 5, the spotlight is the brand new i6 from Li Auto, ending the month in sixth because of a report 29,368 gross sales. Whereas it might be thought of on paper a competitor to the beforehand talked about FCB Tai 7, this can be a extra family-orientated crossover, targeted on consolation, luxurious, and know-how as a substitute of off-road skills. It must be high 5 materials for 2026.

Exterior the highest 5, now we have a number of surprises, beginning with the Geely Galaxy Starship 7 exhibiting up in sixth with a report 16,883 registrations. Count on the glossy midsize SUV to turn out to be the brand new star participant for the model, and it’s most likely hoping to win a few high 5 presences quickly with this one.

Proving that full dimension fashions had been the least affected by the inducement drop, this January now we have eight representatives from this class within the high 20. Moreover the aforementioned fashions, we also needs to spotlight the #10 place of the AITO M8. So, the startup make positioned two fashions on the desk, all whereas Nice Wall’s premium model WEY positioned its giant MPV, the Gaoshan, at #15, and Geely Group positioned two of its three behemoth SUVs within the high 20, with the Rolls-Royce-like Zeekr 9X ending the month at #17 whereas the extra humble Geely Galaxy M9 was #18, with 6,592 registrations.

Nonetheless within the Geely steady, Zeekr positioned a second mannequin on the desk. The 7X midsize SUV exhibiting up at #19, a deserved prize for a mannequin with such a rounded bundle.

Closing the desk, now we have an Aion mannequin. The brand new i60 crossover gave a lot wanted quantity to a make that has seen higher days. Will the i60 change Aion’s fortunes?

Lastly, exterior the highest 20, the highlights come from Wuling. The crossover model of the Wuling Bingo, the Bingo S, ended fewer than 300 models behind the #20 Aion i60, whereas one other Wuling mannequin is ramping up and seeking to be a part of the desk quickly. The Starlight 560 is true to Wuling’s ethos — worth for cash — as this can be a 7-seat compact crossover being bought for $14,000 in its BEV model. It gives a selection of a 60 or 69 kWh LFP battery. Count on this mannequin to be in style, not solely in China, but in addition in a lot of export markets.

Wanting on the total producer rating, now we have shock and awe — Geely (165,000 models) has crushed the competitors and received the January trophy, whereas BYD (69,000) was solely 4th!

Nonetheless extra stunning, #9 Nissan was up 14% YoY in a month when everybody else noticed falling gross sales (besides … Toyota?!? which was up 4%). One wonders if this was only a blip, or if the Japanese make has once more discovered a foothold in China.

Exterior this high 10, a number of mentions are due for the startups, which proceed to develop quick. #12 AITO was up 83% YoY, with 40,000 registrations, whereas #13 Xiaomi was up 70% YoY, with 30,000 registrations. The spotlight, although, was NIO. Because of the brand new ES8, it noticed its gross sales surge 162% YoY, permitting it to be #22 in January, even forward of #26 Tesla (-45% YoY, with 18,500 registrations).

Within the EV producer rating, regardless of dropping half of its share, BYD began the yr prefer it ended the final one, main the desk, with 11.5% share.

BUT … not solely has it seen its market share break up in half; it additionally noticed Geely begin the yr with 10.4% share. So, the highest two are separated by nearly 1%!

And, whereas it’d nonetheless be too quickly to say that Geely will surpass BYD, we might see a race for supremacy in China between these two.

#3 AITO (6.7%) and #4 Xiaomi (6.5%) seemingly got here out of nowhere into the highest 5, whereas final yr’s bronze medalist began this yr two positions under, in fifth, with 5.4% share. True, it’s not the most effective begin of the yr for SAIC’s quantity model, but it surely might have been worse — in any case, 2025’s 4th positioned Tesla (slowly fading into irrelevance) and fifth positioned Leapmotor are nicely under the highest 5….

Simply exterior the highest 5, now we have #6 Xpeng (4.6%), which is hoping to affix the desk quickly.

Wanting on the OEM stage, Geely is even nearer to BYD, with solely 0.3% separating the 2 OEMs. And with Geely firing on all cylinders, anticipate the Taizhou-based OEM to displace BYD someday sooner or later….

SAIC is third, with 9.8% share, taking advantage of the nice outcomes of the MG 4 and Shangjie model. Added to the quantity of the Wuling model, Shangjie allowed the Shanghai OEM to begin the yr in third, one place above of what it had a yr in the past.

Newcomers to the OEM high 5 are #4 Seres, proprietor of the AITO model, and #5 Xiaomi, with 6.7% and 6.5% share, respectively.

That is extra proof that it’s not solely overseas OEMs feeling the warmth. Tier two Chinese language legacy OEMs, like Chery and Changan, are additionally feeling the pinch of their house market and wish good export markets greater than ever with a purpose to steadiness out softening demand at house.

So, BYD and Geely combating for #1 and startups consuming legacy OEMs’ lunch appear to be two high gadgets on the menu for 2026. Please deliver on the popcorn, as a result of this yr must be enjoyable to look at!…

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our each day publication, and observe us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our each day publication for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if each day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage