Echoes From The Previous: What The “Twin Oil Crises” From The Seventies Train Us About The Coming Impacts Of Hormuz’s Blockade.

Assist CleanTechnica’s work by a Substack subscription or on Stripe.

We’re now two months into Trump’s newest imperial journey. The sudden assault on Iran’s management on February 28th (amidst ongoing negotiations between Iran and the US) led to a collection of escalatory measures from either side which have most notably induced the closure of the globe’s most essential vitality hall: the Hormuz Strait.

Hopes for a fast decision of this battle are over and the injury from the closure has compounded by the weeks and rippled all around the world’s financial system. It’s now all however sure that even when the disaster have been to be solved tomorrow one way or the other, the misplaced barrels and broken infrastructure imply we’d require months, maybe years, to get again to any semblance of pre-war normality. And the longer it goes on, the extra that the fossil fuel-based vitality system — and by extent the world financial system — will undergo.

But this isn’t the primary time the world has confronted such an vitality shock. The “twin crises” from the Seventies eerily mimic the double shock of the Russia–Ukraine warfare and the US/Israel–Iran warfare, and due to this, a deeper comparability is price trying into. In spite of everything, those that don’t know their historical past are doomed to repeat it, aren’t they?

For many who might not know what precisely are we speaking about, the “twin crises” have been the Oil Embargo of 1973 and the Islamic Revolution in Iran in 1979, the primary of which ended a protracted interval of very low oil costs and tripled them in a matter of weeks, the second of which compounded on the earlier disruption and introduced oil costs to ranges thought unattainable in these years. Each moments may be clearly seen should you have a look at historic oil costs, adjusting for inflation:

These two crises basically reshaped the world’s financial system. By understanding how that occurred, we will attempt to predict how the present disaster might do the identical.

The Twin Crises, Half I: The 1973 Oil Embargo

In 1973, a number of Arab nations imposed an embargo on the nations supporting Israel’s warfare efforts in the course of the Yom Kippur Warfare, most essential of all the US, which had simply supplied a large weapons carry for the Israelis.

Crucially, this occurred at a important juncture: for many years, the US had been the “swing producer”, able to growing or reducing manufacturing to suit adjustments in World Demand. However by the 1960’s it was clear that US manufacturing couldn’t develop for for much longer, and in 1972 it peaked, that means the US misplaced the potential to be a “swing producer” and, from there on (up till the golden age of fracking within the 2010s), the nation would rely on Center East nations to cowl its thirst for gasoline.

All in all, some 4.5 million barrels, or round 7% of world oil demand, stopped being out there for Western nations (although, they didn’t essentially vanish for the markets), and since US manufacturing had peaked, there was no various supply to produce them. Oil costs promptly reacted, almost tripling from earlier ranges. As seen within the earlier chart, they went from round $26/barrel in right this moment’s {dollars} to round $71 in a matter of 5 months.

That is the story most individuals learn about, however one thing way more essential occurred afterwards. On March 17, 1974, lower than 10 months after it began, the embargo was lifted and Center Jap oil as soon as once more arrived in Western nations… however the value didn’t observe. Costs would keep within the $70–80 vary for the following few years, and would by no means once more attain such low costs on a constant foundation.

The Twin Crises, Half II: The 1979 Islamic Revolution

In 1979, the Sha of Iran was deposed by a generalizes revolt of the Iranian inhabitants, and as an alternative a cadre of spiritual students based the Islamic Republic, a theocratic authorities that has since been governing the nation.

The vitality disaster truly began a bit earlier, in late 1978, when — as a part of the generalized protests taking place within the nation — a strike from Iranian oil employees introduced oil manufacturing down from 6 million barrels a day (mbd) to lower than 1.5. This, alongside misplaced manufacturing after the ousting of the Sha because of overseas professionals leaving, and additional losses down the road attributable to the Iran-Iraq Warfare, meant that at a degree some 5 million barrels have been misplaced — once more, round 7% of world oil demand.

As soon as once more, this meant that the earlier equilibrium broke, and oil costs, already tripling their pre-1973 common, greater than doubled as soon as once more, going from $72 (adjusted for inflation) in early 1979 to a file of $160 in early 1980. Costs wouldn’t come right down to earlier ranges till 1985, and they might by no means once more hover round $25–35 as they did earlier than 1973.

A Courageous New World After The Oil Crunch

The dual disaster basically modified the way in which the World Economic system works.

From the availability aspect, they triggered huge investments in various sources of oil, together with Alaska, Alberta, the North Sea, Venezuela, Brazil, the Caspian Sea, and the Caucasus. This completely broke the affect of Center Jap nations, who went from over 35% of world manufacturing to lower than 25%.

However probably the most fascinating adjustments got here from the demand aspect. Oil demand stagnated for almost a decade, solely surpassing the degrees of 1979 in 1988. Economies pivoted away from oil in each sector the place alternate options existed, primarily electrical energy technology (these have been the years when France’s nuclear fleet was deliberate, with gasoline and coal additionally gaining massively), and there the place oil was important, extra environment friendly strategies of utilizing it have been developed. These have been the malaise years for the US automotive trade, because it couldn’t compete with nimbler, extra environment friendly automobiles coming from Japan and later South Korea, the likes of which grew to become extraordinarily fashionable as gasoline costs stored going up.

There was additionally a major shift in developed economies that moved away from trade — closely reliant on vitality — into companies, thus reducing the general oil required to generate a certain quantity of financial development (that is, the oil-intensity of the financial system). A secondary impact within the medium time period was the implementation of neoliberal insurance policies in lots of nations, most essential of all of the US, which led to an enormous pivot to third-world manufacturing, notably Chinese language, which was closely reliant on coal, greater than oil.

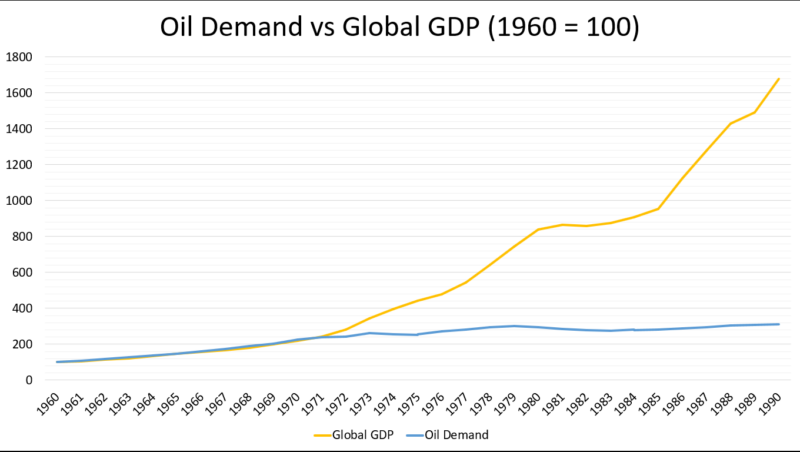

And due to these deep adjustments in the way in which the financial system labored, this led to a number of basic adjustments in development: first, the definitive peak on per-capita world oil consumption, which till then had been rising continuous for many years; second, the definitive peak for the oil-intensity within the financial system:

As seen on this chart, world per-capita oil consumption had been rising steadily for the reason that Sixties (and really for the reason that finish of WWII), but it surely hit a peak in 1973, and regardless of a restoration in 1975–1979, its development ceased completely after 1980, by no means to recuperate.

Likewise, within the years previous to 1973, there’s nearly an actual correlation between the scale of the financial system and oil demand; nevertheless, this development utterly breaks after that 12 months, with financial development successfully decoupling from oil consumption (that is, with a discount within the oil-intensity of the financial system). I lower the graph in 1990 as a result of it diverged much more after that date, making it tough to see the correlation previous to 1973.

With oil demand cratering and important funding in new oilfields, the Eighties have been characterised by a rising oil glut that additional materialized as Saudi Arabia flooded the market in late 1985. This meant repeatedly decrease costs, largely staying between $25 and $55 in right this moment’s {dollars} between 1986 and 2003 … however that didn’t change the basic traits: oil consumption per capita stayed stagnant and the oil-intensity of the financial system stored falling.

Or, in different phrases, the disaster basically reshaped the financial system at a everlasting stage, making a return to the “previous regular” unattainable, whilst oil costs went again down. This lesson, as we are going to see, gives a important perception: a return to normalcy not often means a return to pre-crisis traits.

The 2020’s “Twin Disaster:” The Invasion of Ukraine And The Assaults On Iran

The primary oil disaster in our decade occurred after Russia’s invasion of Ukraine, but it surely was largely a digital one: Russian manufacturing was nonetheless there, it was simply not being bought by nations complying with the US and Europe’s sanctions. Nonetheless, it was sufficient to carry costs to over $120 in some months, averaging $97 for the entire 12 months 2022.

This implies the 2022 disaster was largely a supply-chain disruption. Oil demand had fallen dramatically in 2020 because of the Covid pandemic, forcing producers to close down wells and lower funding in exploration and drilling. By 2022, the financial restoration was in full swing, and oil demand was quickly catching up with sluggish provide (because of the aforementioned cuts on funding), that means when Russia invaded Ukraine, and Europe + the US determined to impose sanctions, there was no various supply to depend on. Nevertheless, that this disruption was digital (and never materials) may be seen in the truth that demand stored rising by 2022 and 2023, going from 97 mbd in 2021 to 102 mbd in 2023.

The 2026 oil disaster, attributable to the US and Israel’s assault on Iran, is lower from a totally completely different material. The Iranian regime responded to the assaults by shutting down the Strait of Hormuz, a important chokepoint that accounts for some 20 mbd coming from the oilfields of Saudi Arabia, Qatar, the UAE, Oman, Iraq, and Iran itself — plus 1 / 4 of the worldwide LNG and a good portion of fertilizer and helium, supplies that may severely disrupt loads of different industries.

However right this moment we’re specializing in oil.

A few of this manufacturing, in all probability round half of it, has been diverted by various routes, primarily Saudi Arabia’s East-West pipeline, the UAE’s Habshan-Fujairah pipeline, and Iraq’s Iraq-Türkiye pipeline. Nonetheless, this implies round 10 million barrels a day, or 9.5% of world demand, have evaporated from the worldwide markets: not like in 2022, this isn’t a digital disaster or a supply-chain disruption, this can be a materials scarcity that should be reckoned with eventually.

As Paul Krugman refers in his Substack, these 10 million barrels of oil a day might want to disappear from world demand, and the value should go up as excessive as required to do the trick. Up to now, in response to the IEA, demand has fallen 800,000 barrels a day in March, and can maintain falling by 2.5 mbd in April, which is a staggering quantity, however nonetheless solely ¼ of what’s wanted to carry steadiness to the markets.

If that is so, then why aren’t costs skyrocketing proper now? It’s arduous to provide a exact reply, however the reason being possible twofold:

- First, there was a major buffer. As a lot as a billion barrels might have been launched from storage by the OECD and China, plus there have been “barrels in storage” within the sea from sanctioned Iranian and Russian oil and from common vessels transporting crude, a few of which departed earlier than the blockade began and have simply arrived of their vacation spot within the final couple weeks. Additionally, should you keep in mind our articles about Oil Demand from final 12 months, oil manufacturing was forecasted to be over 2mbd in extra of demand this 12 months.

- Second, the market stays stubbornly optimistic in a sudden decision of the blockade. This may be seen in oil futures, that are these days some $30 cheaper than bodily barrels for instant supply.

However this could solely purchase the world a lot time. Finally, both manufacturing will ramp as much as meet these 10 million lacking barrels (which, except the Strait is absolutely reopened, is just not doable), or demand should come right down to these ranges.

Echoes of the previous: classes to be realized and penalties to be anticipated.

As Mark Twain stated, historical past doesn’t repeat itself, but it surely usually rhymes.

6 years handed between the Oil Embargo and the Islamic Revolution; 4 handed between Russia’s invasion of Ukraine and the US/Israel assault on Iran. In each circumstances, the results from the previous disaster compounded within the latter; in each, the latter had a extra direct and materials influence than the previous; and if I could take out my crystal ball, in each the world was (or might be) modified without end.

The 1973s oil disaster brings a primary lesson, and maybe probably the most fascinating one: even when a disaster ends, it might carry a brand new regular. Costs didn’t return down after the top of the oil embargo, and even within the depths of the oil glut of the Eighties, it solely sometimes reached the low ranges that had been the norm within the pre-1973 world.

That is one thing very prone to repeat this time. The elements which have stored the market afloat on this disaster, primarily associated to huge storage that didn’t exist in 1973, are additionally prone to maintain strain on demand in years to come back. Even when the strait was reopened tomorrow, oil tankers must return all the way in which, replenish, and restart their routes, that means bodily oil received’t arrive at its vacation spot till late Could or June. OECD and Chinese language storage may even need to be replenished: at 400 million barrels to date for the OECD, that may require an extra oil manufacturing of two mbd for 200 days, and since China has in all probability launched an identical quantity, and since US storage was already low when this disaster began, we’re at finest two years away from the pre-war base.

The Seventies additionally introduced important adjustments in world oil geopolitics. The Center East misplaced floor, and new areas grew to become essential gamers, most essential of all of the USSR, but additionally the US and Northern Europe. This time, it appears South America may very well be one of many most important beneficiaries, in addition to US shale and Alberta’s tar sands, which have been having some monetary points previous to the disaster.

However maybe probably the most fascinating classes may be present in oil demand and everlasting adjustments within the financial construction of the world. Again within the Seventies, the disaster triggered huge investments in various sources of vitality and extra environment friendly technique of utilizing no matter oil was out there: merely one month into our disaster, we’re already seeing booming EV gross sales in lots of markets and traditionally excessive exports for Chinese language photo voltaic panels.

Again within the Seventies, the oil disaster was sufficient to completely change the trajectory of a number of European cities, most notable of all Amsterdam, which took a pro-bike path ever since, stopping the usage of in all probability billions of barrels of oil by the final 5 a long time. We don’t understand how lengthy this disruption will final, however the longer it’s, the deeper the consequences might be felt, and we’re previous the purpose the world may return to the pre-war normality in any case.

The identical, however completely different

Again within the Seventies, there have been only a few alternate options for oil in transportation, and thus the adjustments that introduced oil demand right down to the fabric provide ranges needed to do with coverage (corresponding to velocity limits), effectivity (corresponding to these smaller, extra environment friendly Japanese automobiles), and urbanism (corresponding to investments in public transportation and bike-friendly cities). These alternate options, although extraordinarily essential, may solely go to date, and demand for gasoline for highway transportation has elevated lots since 1979.

However in areas the place there have been alternate options, the adjustments have been fast and everlasting. Oil was once a most important a part of electrical energy technology, and by the ’80s it had been all however deserted, as nuclear, gasoline, and coal made up for higher alternate options: right this moment, oil represents a mere 2.6% of world electrical energy manufacturing.

The distinction is that this time we have now loads of alternate options we didn’t have within the Seventies, and specifically, that transport that might not be viably electrified in that decade may be right this moment. This implies there’s an opportunity this warfare will break the proverbial again of oil, accelerating the development in direction of mobility alternate options fueled by a Chinese language trade that for a few years was accused of “overcapacity” however that these days can provide as many EVs and photo voltaic panels because the world wants.

Whereas the Seventies twin crises broke the development and introduced us a peak in per-capita oil consumption and a far much less oil-intensive financial system, I consider the 2020s twin crises have the potential of ending oil demand development for good. That is one thing mirrored in a number of oil and vitality retailers I observe, which this week began warning about everlasting demand destruction if the disruption is just not over quickly. In fact, the longer the warfare, the extra dramatic the influence, however I consider two months (plus the 2 years it is going to take us to recuperate from these two months) might be sufficient to create a shift, regardless that each week that this disruption stays that shift will speed up.

Oh, and naturally, all of this additionally applies for LNG, which can really feel extra strain from photo voltaic panel deployment as nations discover out, as soon as once more, how harmful it’s to rely for the premise of your financial system on a overseas product you don’t have any management over.

However a final query stays. Will demand destruction proceed as soon as the crises finish? Will EV development lower into oil demand quick sufficient to beat different sources of development? And if this occurs, will we see oil costs plummet?

As a result of, see, the final disaster additionally ended oil value stability. What was once a predictable and regular market grew to become a curler coaster of highs and lows. So given the doable situation I simply introduced, an extra influence of thes crises may very well be much more volatility because the market violently pivots between oversupply and shortage.

This might imply some very unhealthy years sooner or later for Massive Oil … one thing ironic if we expect that every one this mess was delivered to us by probably the most pro-oil candidate in a technology.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our every day e-newsletter, and observe us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage