Help CleanTechnica’s work by means of a Substack subscription or on Stripe.

The European passenger plugin automobile market scored 298,000 registrations in January, a development of twenty-two% YoY. Positively, BEVs (195,000 items, +16% YoY) continued to develop regardless of the drop in EV incentives in sure markets. However the spotlight of the month was plugin hybrids (PHEVs), as they jumped 33% yr over yr (YoY) to some 102,000 items, or 10% share of the whole market, which is their highest development fee in January since 2021. A very good omen for the remainder of the yr?

Whereas plugins had been up, the general market had a sluggish month (-4% YoY, to rather less than a million items), beginning 2026 BEV share at a robust 20%, larger than the 17% of final yr, the 12% of January 2024, and the ten% of the earlier yr. Which means that the BEV share doubled in simply three years. So … will we see 40% BEV share in January 2029? And 80% in January 2032? One can solely dream….

Relating to different powertrains, whereas petrol (-26% YoY) and diesel (-22% YoY) are in freefall (at this tempo, count on diesel new automobile gross sales to finish round 2029…), plugless hybrids are (nonetheless) rising, going up from 35% share in January 2025, to their present 39% share.

Additionally, this meant that 69% of all passenger autos offered in January in Europe had been electrified (to some extent), strong development from the 59% rating of a yr in the past. At this tempo, count on all new automobile gross sales in Europe to be electrified, in some type, by 2030.

Nonetheless, count on the 20% BEV share to be a baseline, with the BEV market rising its share all year long and ending the yr near 25% share.

In January, we obtained a really various prime 5, with 5 totally different OEMs represented, coming from 5 totally different international locations. An indication of issues to return?

Carry on the popcorn, as a result of the following few months will certainly be enjoyable to look at!

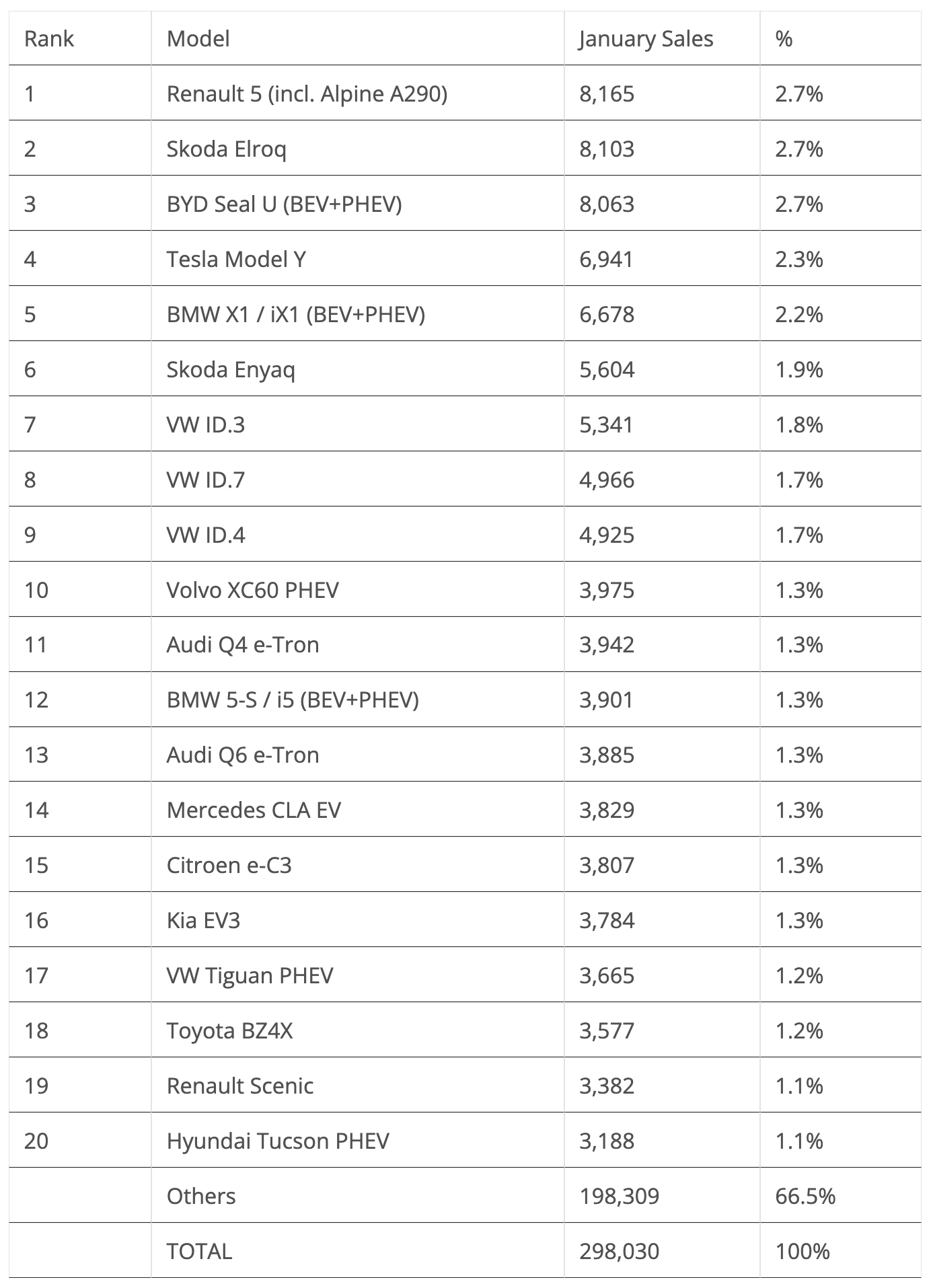

Wanting on the month-to-month mannequin rating:

#1 Renault 5 / Alpine A290 — After an exciting race with the #2 Skoda Elroq and #3 BYD Seal U (all three ended separated by simply 102 items), the French twins began the yr with a win, scoring 8,165 registrations final month, which allowed them to begin within the lead. Positive, don’t count on this result in final — apart from the specter of the aforementioned Czech and Chinese language fashions, in March, count on the Tesla Mannequin Y coming all weapons blazing into #1. BUT. A podium result’s absolutely on the playing cards in 2025, and possibly the French EVs may have a shot at displacing the Skoda Elroq from the runner-up spot, bettering on its bronze medal achieved in 2025.

#2 Skoda Elroq — The 8,103 deliveries of January didn’t permit it to begin the yr within the management spot, however that is however a great rating. However with the upcoming sibling, the very promising Epiq small crossover, touchdown within the second half of the yr, one wonders if the Czech mannequin will proceed to be a frequent presence on the rostrum. Having been second place in 2025, Skoda’s crossover should work onerous to remain on the rostrum, not solely due to the Epiq’s inner competitors, but in addition as a result of the exterior competitors is changing into ever extra fierce.

#3 BYD Seal U (BEV+PHEV) — The Chinese language SUV hit 8,063 registrations final month, which means that whereas the BYD veteran star is already fading in China (it was solely ninth in its residence market this month), in Europe it’s nonetheless podium materials (a bit like when veteran soccer/soccer gamers #ahem# Cristiano Ronaldo #ahem# depart the highest leagues and semi-retire in much less aggressive leagues…). January’s third place end was a lot due to beneficiant reductions, however nonetheless, with the mannequin’s growth prices now effectively behind it, BYD can afford to enter onerous low cost territory with this one.

#4 Tesla Mannequin Y — The made-in-Germany crossover was 4th in January, with 6,941 registrations, up 19% YoY (however down 39% in comparison with January ’24). With the refreshed model nonetheless recent, the Mannequin Y remains to be hanging on, one thing that the Mannequin 3 can not say (with 1,041 items, it had its worst consequence since July ’22). Tesla will attempt to preserve its crossover within the prime positions for so long as it may. Nonetheless, whereas the Mannequin Y ought to preserve its finest vendor crown this yr, the Mannequin 3 can have a tough time staying within the prime 5.

#5 BMW X1 PHEV / iX1 — With the Neue Klasse BEVs excessive on BMW’s priorities record, one could possibly be forgiven for forgetting that BMW already has a few quantity promoting EV fashions. And the perfect of them are the X1 PHEV / iX1 duo, each primarily based on the X1 ICE mannequin. The reality is that the compact SUV twins hit 6,678 registrations final month, permitting them to affix the highest 5. With a deep, Neue-Klasse-inspired refresh coming this yr, count on the twins to proceed promoting in massive numbers. How massive? Exhausting to say in the meanwhile, but when the refresh is something as profitable because the upcoming iX3, then we could be speaking about podium materials, or no less than a prime 5 presence.

Simply outdoors the highest 5, a point out is due for the Volkswagen Group prepare behind the frontrunners, with 4 representatives (Skoda Enyaq, VW ID.3, VW ID.7, and VW ID.4) between the sixth place and the ninth place, in addition to the Audi This autumn in eleventh and the Audi Q6 in thirteenth — which, added to the 2nd place of the Skoda Elroq, locations 7 Volkswagen Group fashions within the prime 13 spots. Wow. That’s BYD stage of domination there….

The opposite highlights are the BMW 5 Sequence PHEV/i5 twins, which jumped into the twelfth place, successful the total dimension class. All whereas the Mercedes CLA EV continued to experience its wave of success, accumulating one other prime 20 spot, this time in 14th.

Relating to new faces, the Citroen e-C3 EV is again on the desk, at #15, as evidently Stellantis now really needs to promote the mannequin. The refreshed Toyota BZ4X joined the highest 20, in 18th. (Is the Japanese large waking up in Europe?). Additionally, as a little bit of a shock, this time Renault positioned a second mannequin on the desk, with the Scenic crossover sneaking in at #19. Is the success virus spreading in Renault’s lineup?

Outdoors the highest 20, the spotlight was the Chinese language Jaecoo 7 PHEV, which ended the month in twenty first, just some 30 items behind the #20 Hyundai Tucson PHEV. This proves that it’s not solely MG, BYD, and Geely which might be successful within the European market. Different, smaller Chinese language gamers are gaining floor in Europe as effectively, and with total gross sales stagnating, these conquest gross sales are on the expense of somebody….

Wanting on the highlights from the mainstream manufacturers rating, the perfect performer was #20 BYD, which grew 173% YoY to shut to 18,000 gross sales. Whereas the Shenzhen OEM is faltering in its home market, in Europe the image is sort of totally different, ending the month fewer than 1,000 items behind MG, China’s longstanding gross sales champion in Europe, and 10,000 items forward of #27 Tesla(!), which dropped by 17% YoY.

Anticipate BYD to beat each manufacturers this yr, changing into Europe’s largest market disruptor.

On the losers aspect, we’ve got three surprises, with #14 Dacia dropping by 35% YoY (already a sufferer of an ICE melting occasion?), and the Koreans Kia (ninth, down 19% YoY) and Hyundai (tenth, down 20%) dropping as effectively. These adjustments don’t appear to have a straightforward clarification. Is that this a blip? One thing to take a look at within the coming months.

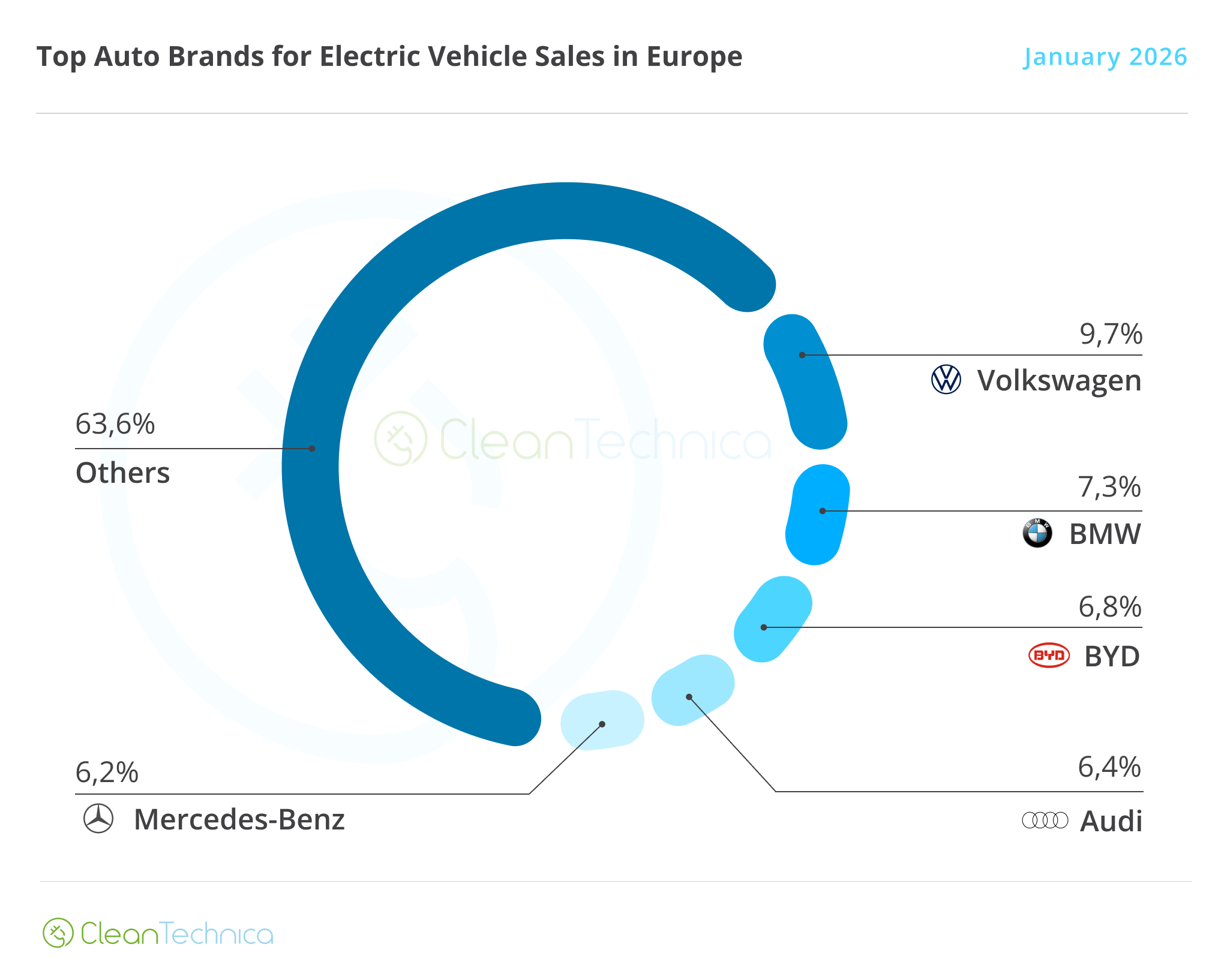

Within the EV producer rating, Volkswagen has saved the management place, however it has began out from a decrease base than 12 months in the past. In January 2025, it had 11.1% share. This January it was at 9.7%. I imply, it’s nonetheless good, however the VW ID.Tiguan and ID.Polo are wanted to ramp up volumes if the German make needs to finish this yr with the identical share it ended 2025 (11%).

BMW (7.3%) began the yr in its standard place, the runner-up spot, adopted by the most important shock of the highest 5. BYD seemingly got here out of nowhere and jumped into third place! Germans (and everybody else), beware. BYD has formally turned a pressure to be reckoned with in Europe, succeeding Tesla in that position.

Talking of the Texan make, Tesla (2.7% share, down from 4% in January ’25) continues to slip into irrelevance, to the purpose that it’s now not even the #1 US EV maker in Europe! A slowly progressing Ford (3.6% share in January) has managed to overhaul it! Positive, Tesla ought to bounce large in March and will surpass Ford by then, however … presently, Tesla has been relegated to competing with Ford for a place within the pack. Management positions at the moment are a distant reminiscence for the US model.

Outdoors the highest 5, the spotlight is #7 Renault (5.4%, up from 4% in January ’25), which is trying to surpass an additionally progressing #6 Skoda (5.7%) to attempt to be a part of the highest 5 someday this yr.

As for OEMs, Volkswagen Group began the yr in entrance (unsurprising, actually) with 26.4% market share. With nearly all manufacturers from Volkswagen Group posting robust ends in the EV class, Volkswagen Group will attempt to preserve its market share between 25–30%…. Do you assume this shall be potential?

Stellantis (10.4%, up from 9.5% in January ’25) is the brand new #2, having changed BMW Group (8.9%) in that place. The German OEM is ready for quantity deployment of its new iX3 to have one other shot on the second spot.

With Stellantis in every single place, making an attempt on one hand to actively promote its EVs whereas on the similar time (re)introducing diesel variations of some of its fashions (that model new, and rising, know-how…), BMW is ready to get well runner-up standing from the multinational conglomerate.

Hyundai–Kia (8%) began the yr in 4th, however it might want to preserve a detailed eye on #5 BYD (6.9%). Due to success tales in much less media-friendly markets (in January alone, it had 1,000 gross sales in Azerbaijan, 1,000 in Eire, 600 in Poland, 500 in Portugal, 500 in Ukraine, and 400 in Albania), it’s leaping positions and will change into a podium candidate already this yr!

Under these OEMs, and in a reverse state of affairs of what’s occurring in China, Geely (6.7%, down from 8.6% in January ’25) is experiencing the other dynamic as BYD. It’s dropping vital share in Europe. In January, Geely suffered from Volvo’s sluggish begin, however no matter that, Geely wants a quantity model to shore up its market share. The namesake model will have to be shortly deployed in Europe, and its lineup expanded — specifically with fashions just like the small Xingyuan, set to be known as the EX2 in Europe.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our every day e-newsletter, and comply with us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our every day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on prime tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage